Budgeting Strategies

50/30/20 Budget Rule for Couples: A Practical Guide (2026)

The 50/30/20 budget rule adapted for couples. Learn how to split needs, wants, and savings when two incomes, two spending styles, and shared financial goals collide.

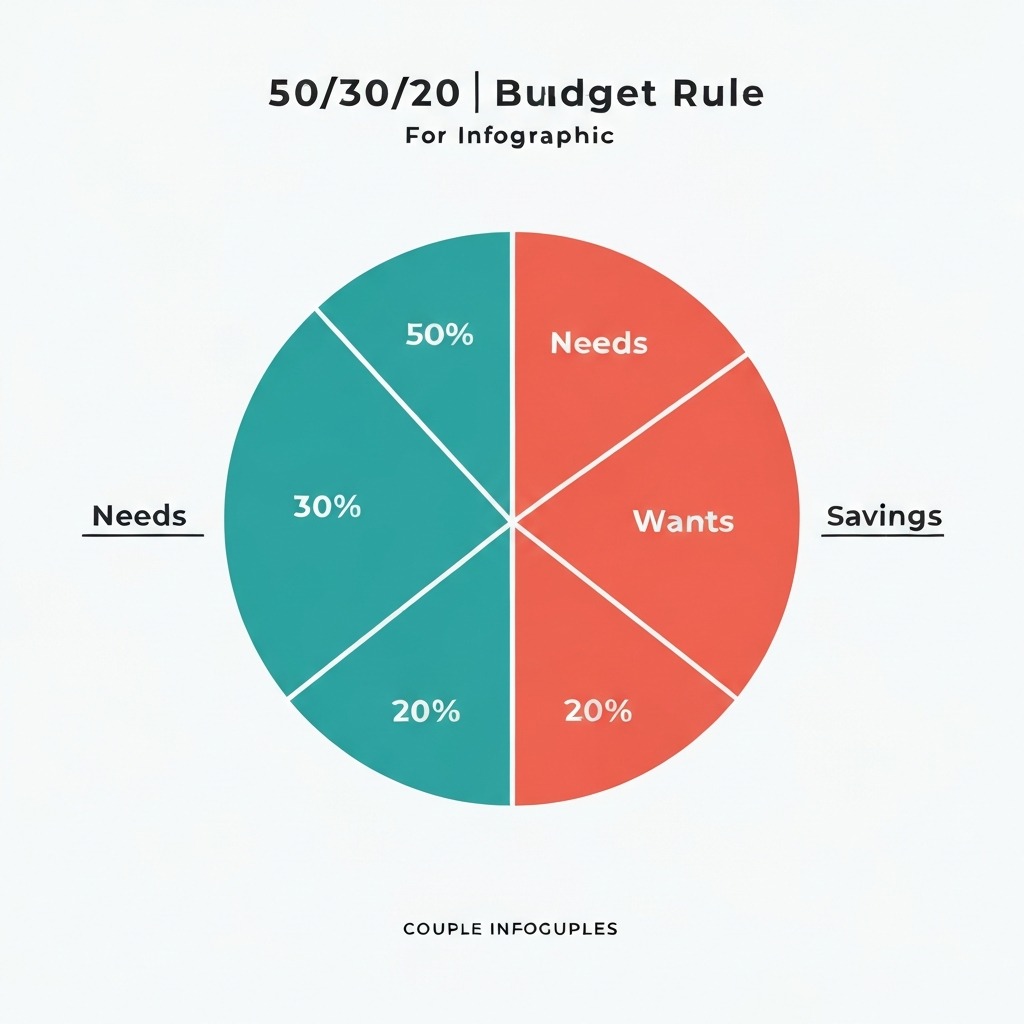

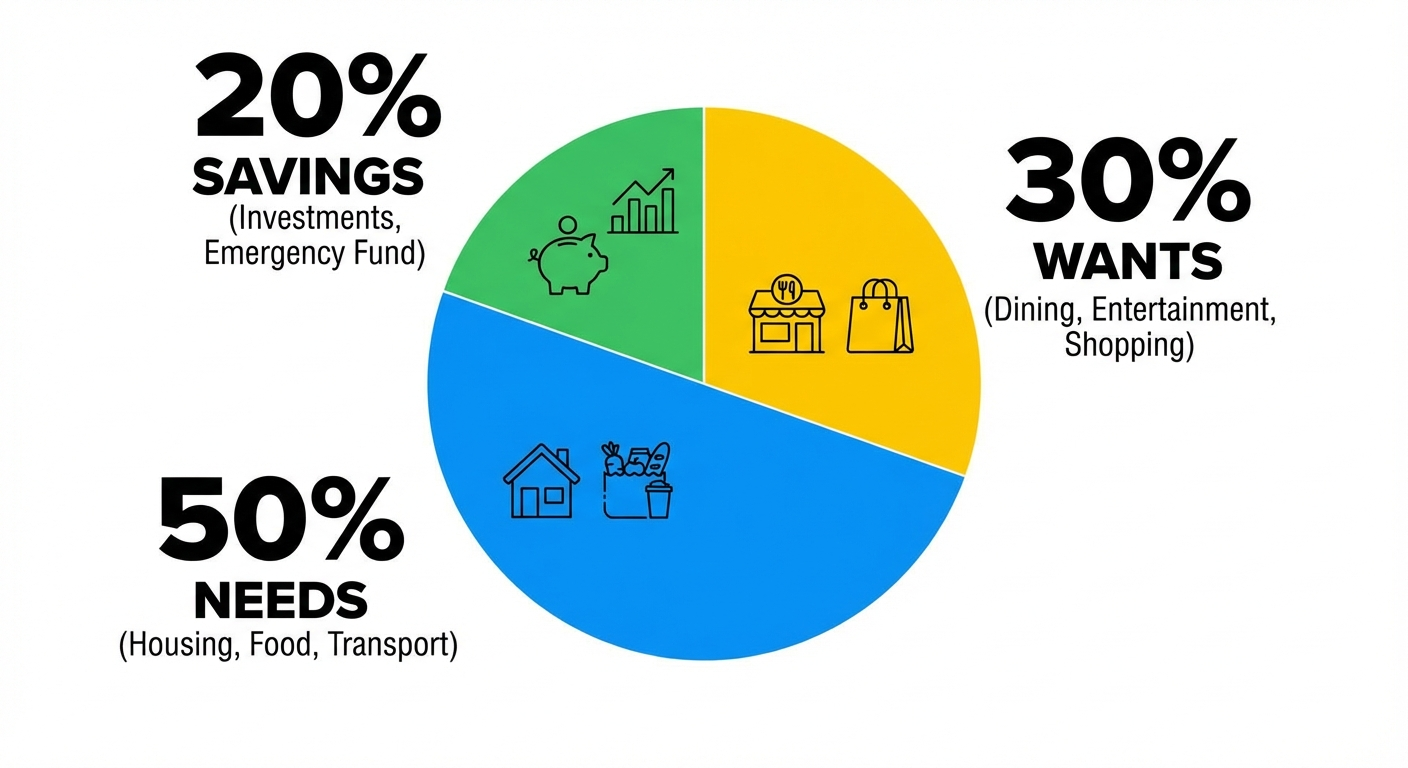

The 50/30/20 budget rule allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt. For couples, the rule works best when applied to combined household income with agreed-upon shared and individual spending categories — eliminating the money arguments that undermine most couples' financial plans.

By Rachel Torres, Content Specialist | Last updated: March 2026

Table of Contents

- What Is the 50/30/20 Rule?

- Adapting It for Two Incomes: The Couples Version

- Defining Needs, Wants, and Savings as a Couple

- The Joint Account Model That Works

- Step-by-Step: Setting Up Your Couple's 50/30/20 Budget

- When the Math Does Not Work: Adjustments for Real Life

- Common Couple's Budgeting Mistakes

- Tools to Track Your Budget Together

- FAQ: 50/30/20 for Couples

- Sources and Methodology

What Is the 50/30/20 Rule?

The 50/30/20 rule was popularised by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. It offers a simple, memorable framework for managing personal finances without the complexity of tracking every expense category.

The basic formula is straightforward:

- 50% to Needs: Housing, utilities, groceries, insurance, minimum debt payments, transportation to work

- 30% to Wants: Dining out, entertainment, subscriptions, shopping, holidays, upgrades

- 20% to Savings and Debt: Emergency fund, retirement contributions, additional debt payoff, investment accounts

The percentages apply to after-tax income — your take-home pay, not your gross salary. This distinction matters significantly: a household earning $120,000 gross may take home $90,000 after federal, state, and Social Security taxes, making that the base for all calculations.

The rule's genius is its flexibility. Unlike zero-sum budgets that require tracking every dollar, the 50/30/20 framework sets guardrails that keep your finances on track while leaving room for human behaviour. You do not need to justify every coffee purchase. You just need to stay within your 30% wants allocation.

Why It Works Long-Term

Most people abandon detailed budgets within 2-3 months because the administrative burden outweighs the benefit. The 50/30/20 rule requires checking three numbers instead of forty. That simplicity creates sustainability — the most important property of any financial system.

Research from the National Foundation for Credit Counselling (NFCC) consistently shows that people who maintain any budgeting system — even an imperfect one — achieve significantly better financial outcomes than those who track nothing. The 50/30/20 rule is imperfect, but it is maintainable.

Adapting It for Two Incomes: The Couples Version

The 50/30/20 rule was originally designed for individuals. Applying it to a two-person household introduces complexity that most guides gloss over. Here is what actually changes:

Use Combined Household Income

The most important adaptation: apply the percentages to combined after-tax household income, not individual salaries.

Why this matters: If Partner A earns $6,000/month and Partner B earns $2,500/month, applying 50/30/20 individually creates wildly different absolute amounts — and often resentment when shared expenses are split equally despite unequal incomes.

Combined household income = $8,500/month

- 50% Needs = $4,250

- 30% Wants = $2,550

- 20% Savings = $1,700

This treats the household as a single financial unit — which, practically speaking, it is.

Proportional Contribution vs. Equal Splits

When combined income goes into the budget, you need to decide how each partner contributes to shared expenses. Two fair models:

Equal split: Each partner puts the same dollar amount into shared accounts. Simpler to manage. Can feel unfair if incomes are significantly different.

Proportional split: Each partner contributes a percentage of their income that equals their share of household income. Partner A (71% of household income) contributes 71% of shared expenses. Partner B contributes 29%.

For most couples with income differences greater than 25%, the proportional model creates less friction and better reflects the reality that shared fixed costs (rent, utilities) are inherently less burdensome for higher earners.

Personal Wants Money Is Not Negotiable

This is the rule most commonly violated and most important to maintain: each partner should have a personal "no questions asked" spending allowance from the wants bucket.

Money arguments often trace back to one partner feeling judged or surveilled about personal spending. If Partner A buys a $40 book and Partner B challenges it, you have created a surveillance dynamic that will corrode trust faster than any overspending.

Set equal personal discretionary amounts — even if total incomes differ. This is not about proportionality; it is about autonomy and dignity.

Defining Needs, Wants, and Savings as a Couple

The biggest fights in couples' budgeting are usually about categorisation, not amounts. Is streaming a need or a want? Is the gym membership a need (health) or a want (optional)?

Sit down together and categorise your current expenses before setting budget amounts. Here is a framework:

Needs (Target: 50%)

These are expenses where non-payment causes immediate, serious harm — shelter loss, legal consequences, or inability to function.

Shared needs examples:

- Rent or mortgage (primary home only)

- Utilities: electricity, gas, water, internet (basic plan)

- Groceries (not restaurants — those are wants)

- Minimum payments on shared debt

- Car payment and insurance (if required for work)

- Basic health insurance premiums

- Childcare (if both partners work)

- Pet food and essential veterinary care

Common misclassifications to watch:

- Subscriptions (Netflix, Spotify): these are wants, not needs

- Gym memberships: wants, unless medically prescribed

- Premium phone plans vs. basic phone service: only basic is a need

- Dining out: always a want, regardless of convenience

Wants (Target: 30%)

Wants are anything lifestyle-improving but not essential to baseline function.

Shared wants examples:

- Restaurants and takeaways

- Entertainment (concerts, movies, sporting events)

- Travel and holidays

- Subscriptions (streaming, magazines, apps)

- Home décor and non-essential furniture

- Gifts beyond agreed minimums

- Hobby expenses

Individual wants (from personal spending allowance):

- Each partner's personal clothing beyond basics

- Personal beauty/grooming beyond basics

- Books, games, personal hobbies

- Individual meals out with friends

Savings and Debt Reduction (Target: 20%)

This category should be treated as a non-negotiable expense, not what is left over at month's end.

Priority order:

- Emergency fund (target: 3-6 months of shared expenses)

- Employer-matched retirement contributions (to capture full match — this is free money)

- High-interest debt elimination (anything above 7% APR)

- Additional retirement contributions (aim for 15% total household income long-term)

- Short-term shared savings goals (house deposit, car, holiday fund)

The Joint Account Model That Works

The three-account model is the most friction-free structure for most couples:

Account 1: Joint Shared Account Receives proportional contributions from each partner. Pays all shared needs (rent, utilities, groceries, insurance, minimum debt payments). Both partners have visibility and equal authorisation.

Account 2: Joint Savings Account Receives the 20% savings contribution. Used for emergency fund, shared savings goals, and retirement transfers. This should be a separate account from day-to-day checking — separation creates psychological distance from spending temptation.

Account 3A & 3B: Individual Personal Accounts Each partner retains personal after-tax income beyond their shared contributions. This funds their personal wants allocation — no scrutiny, no justification required.

Setting Up Automatic Transfers

Manual transfers fail. Automate every movement on payday:

- Direct deposit or standing order to joint shared account (each partner's fixed contribution)

- Automatic transfer to joint savings account (20% of combined income)

- Remainder stays in personal accounts

When money moves before either partner sees it in their personal account, it effectively does not exist as temptation. This single step eliminates most savings failures.

Step-by-Step: Setting Up Your Couple's 50/30/20 Budget

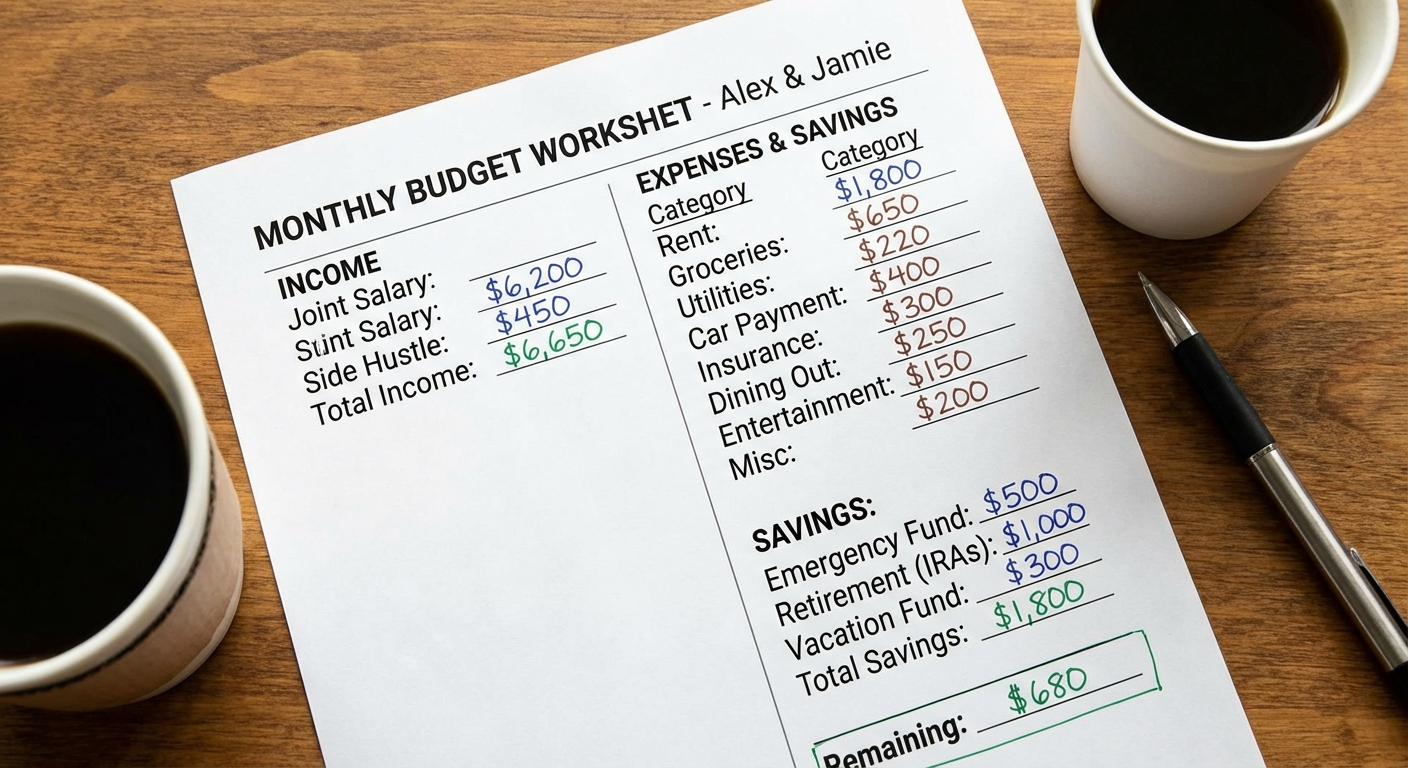

Step 1: Calculate Combined After-Tax Income

Add both partners' monthly take-home pay. Include any reliable additional income (rental income, regular freelance) but exclude bonuses and irregular income from this baseline — budget those separately when received.

Example:

- Partner A take-home: $4,800/month

- Partner B take-home: $3,200/month

- Combined: $8,000/month

Step 2: Calculate Target Amounts

- 50% Needs: $4,000

- 30% Wants: $2,400

- 20% Savings: $1,600

Step 3: List All Current Monthly Expenses

Pull three months of bank and credit card statements. Categorise every expense as needs, wants, or savings. Be honest — people typically undercount wants by 30-40%.

Step 4: Compare Actuals to Targets

Most couples discover one of three patterns:

- Needs over 50%: Usually housing or debt. Requires structural change (lower rent, income increase) or temporary rule adjustment.

- Wants over 30%: The most common issue. Usually lifestyle inflation that crept in unnoticed. Address category by category.

- Savings under 20%: Often a consequence of wants overspending, but sometimes structural — income genuinely insufficient for the current lifestyle.

Step 5: Agree on Changes Together

Do not present a unilateral budget to your partner. Co-create it. Each partner should have equal voice in how cuts are made and which financial goals to prioritise.

For household-wide savings opportunities, meal planning deserves special attention. planfamilymeals.com offers practical weekly meal planning guides that many couples use to stay within their grocery budget — food is one of the most controllable budget categories for most households.

Step 6: Set Up Accounts and Automations

Open joint shared and savings accounts if you do not have them. Set up automatic transfers on payday. Use a shared budgeting app for visibility.

See our best budgeting apps for couples roundup for the tools we recommend for each account structure type.

Step 7: Monthly Review (30 Minutes)

Review three numbers: actual vs. target for needs, wants, and savings. Identify any category that ran over and why. Adjust the following month proactively.

When the Math Does Not Work: Adjustments for Real Life

The 50/30/20 rule is a guideline, not a law. Real life introduces complications that require deliberate adjustment.

High Cost-of-Living Areas

In cities like San Francisco, New York, Sydney, or London, housing alone can consume 40-45% of after-tax income. Squeezing needs into 50% is genuinely impossible for median earners. Adapted frameworks:

- 60/20/20: Needs 60%, Wants 20%, Savings 20%. Appropriate when housing costs are unavoidably high. Does not compromise savings rate.

- 65/15/20: Needs 65%, Wants 15%, Savings 20%. A temporary measure during the highest-pressure income period, with a clear plan to improve.

The savings rate is the last place to cut, not the first. Sacrificing retirement contributions in your 30s to maintain a wants budget you cannot afford is financially catastrophic long-term.

One Income (Temporarily or Permanently)

When one partner leaves work — parental leave, career transition, health — the household effectively operates on one income. Options:

- Apply the rule to the single income for the duration (likely requires cuts to wants)

- Use savings to maintain lifestyle for a defined period (set a hard limit, typically 6 months)

- Adjust all three targets to reflect the reduced income baseline

Significant Debt

If either or both partners carry high-interest debt (student loans, credit cards, car loans above 6%), the 20% savings category should prioritise debt elimination before investment. The guaranteed return of paying off a 19% credit card beats any investment return.

The exception: always contribute enough to your employer-matched retirement account to capture the full match. A 50% or 100% employer match is a guaranteed, immediate return that no debt payoff can beat.

Common Couple's Budgeting Mistakes

Mistake 1: Budget as Punishment, Not Planning

The most common failure mode: one partner presents the budget as a set of restrictions on the other's spending. This creates an adversarial dynamic that dooms the system. Budget together, not at each other.

Mistake 2: No Personal Spending Autonomy

If every dollar must be justified to your partner, the budget will be resented and eventually abandoned. Equal personal spending allowances — even if small — are non-negotiable for long-term compliance.

Mistake 3: Not Accounting for Annual Expenses

Car registration, insurance renewals, holiday spending, and birthday gifts are predictable but often "forgotten" in monthly budgets. Divide annual expenses by 12 and include in monthly allocation.

Mistake 4: Lifestyle Inflation Without Recalculation

When income increases, wants spending tends to scale up automatically. Revisit the budget percentages deliberately with each income change. Ideally, direct at least 50% of any raise to savings.

Mistake 5: Using Credit Cards as Wants Overflow

Credit card debt is among the most financially destructive forces in couple finances. If wants spending regularly exceeds the 30% allocation and lands on a card, the system is broken. The fix is reducing wants categories, not increasing available credit.

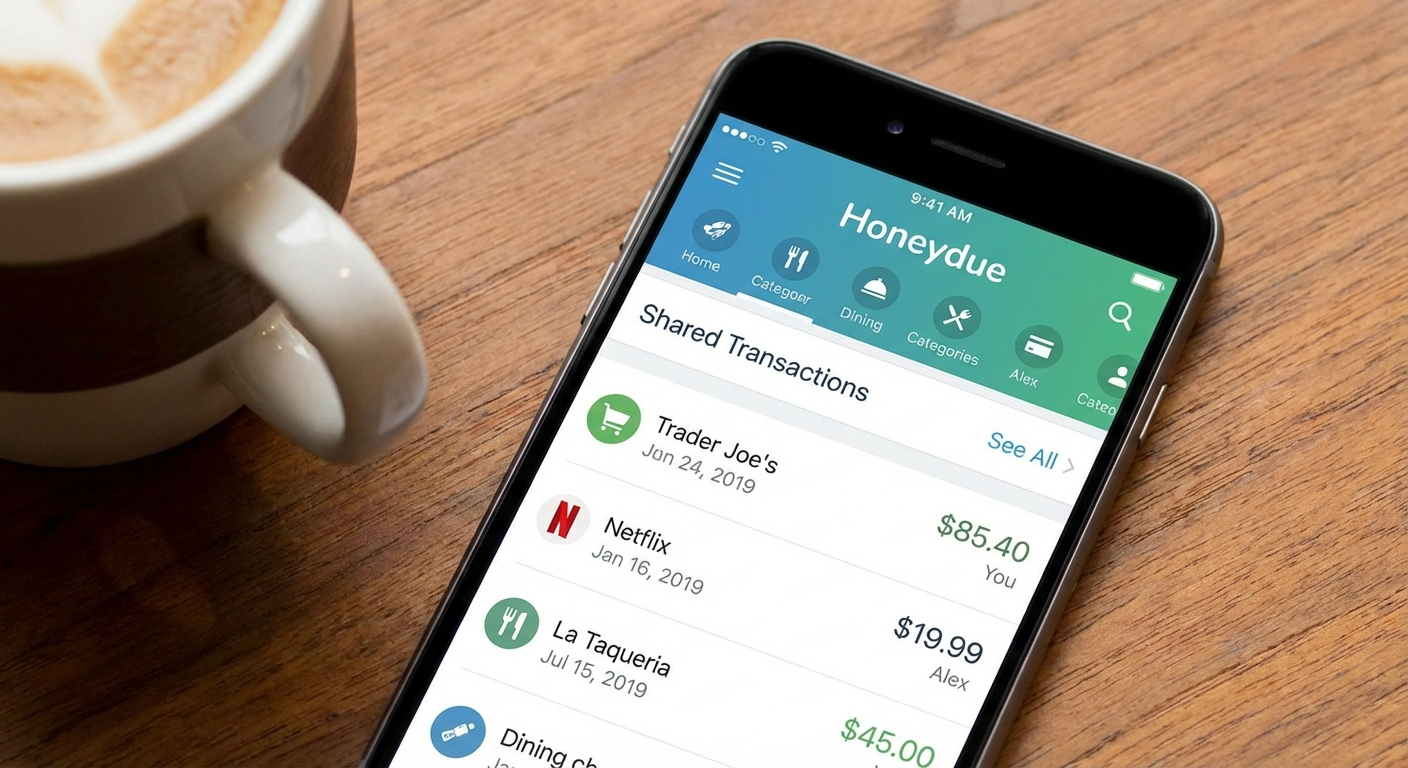

Tools to Track Your Budget Together

YNAB (You Need a Budget)

Best for couples serious about zero-sum budgeting. Real-time sync. Steep learning curve but powerful accountability features.

$14.99/month or $99/year

Monarch Money

Built specifically for couples and families. Clean dashboard, shared net worth view, financial goal tracking. Best overall for couples.

$14.99/month

Copilot

iOS-first, beautifully designed. AI-categorisation with manual override. Excellent for couples who want a minimal-touch approach.

$12.99/month

Google Sheets (Custom)

Free and infinitely flexible. Many couples use a shared template with three summary rows: needs actuals, wants actuals, savings. No learning curve.

Free

For a detailed comparison of apps, see our best budgeting apps for couples review — we tested each with a real two-income household.

FAQ: 50/30/20 for Couples

How does the 50/30/20 rule work for couples with different incomes? Apply the percentages to your combined household income. A couple earning $5,000 and $3,000/month has $8,000 combined — meaning $4,000 for needs, $2,400 for wants, and $1,600 for savings.

What counts as a need vs want? Needs are expenses you cannot avoid without serious consequence: rent, utilities, groceries, minimum debt payments, insurance. Wants are discretionary. When in doubt, ask: could we survive comfortably without this for 30 days?

Should couples use joint or separate accounts? The hybrid three-account model works best: one joint account for shared needs, one joint savings account, and individual accounts for personal wants.

What if our needs exceed 50% of income? Adjust to 60/20/20 or 65/15/20 if necessary, but protect the 20% savings rate. The exact percentages matter less than the principle.

How often should couples review their budget? Monthly in the first 3-6 months, then quarterly once stable. Major life changes require an immediate full review.

Sources and Methodology

Research for this guide draws on personal finance literature, behavioural economics research, and practical budgeting data.

-

Warren, E., & Tyagi, A.W. (2005). All Your Worth: The Ultimate Lifetime Money Plan. Free Press. Original source of the 50/30/20 framework.

-

National Foundation for Credit Counselling (NFCC). (2023). Consumer Financial Literacy Survey. Annual survey of American household budgeting behaviours and outcomes.

-

Consumer Financial Protection Bureau (CFPB). (2024). Financial Well-Being in America. Federal data on household financial security and budgeting adoption rates.

-

Thaler, R.H., & Sunstein, C.R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. Penguin. Behavioural economics foundation for automatic saving and default rules.

-

Klontz, B., Kahler, R., & Klontz, T. (2016). Facilitating Financial Health: Tools for Financial Planners, Coaches, and Therapists. NUCO Publishing. Research on financial conflict patterns in couples.

-

Vanguard Research. (2023). How America Saves. Annual report on retirement savings behaviours and employer match capture rates.

-

Fidelity Investments. (2024). Couples and Money Study. Survey of financial communication patterns and conflict in partnered households.

Rachel Torres is a content specialist focused on personal finance and couples' money management. She has spent six years researching budgeting systems and household financial planning, with particular expertise in the behavioural dynamics of two-income households.