Free Couples Budget Planner

The ultimate budget planner for couples — enter your incomes, track expenses, set savings goals, and start managing money together.

Monthly Expenses

Spending Breakdown

- Rent / Mortgage$1,80040.0%

- Utilities$3006.7%

- Groceries$60013.3%

- Transport$4008.9%

- Insurance$2004.4%

- Entertainment$2004.4%

- Savings$50011.1%

- Debt Repayment$2004.4%

- Personal (Partner 1)$1503.3%

- Personal (Partner 2)$1503.3%

Total Income

$7,500/mo

Total Expenses

$4,500

Surplus

$3,000

Savings Rate

6.7%

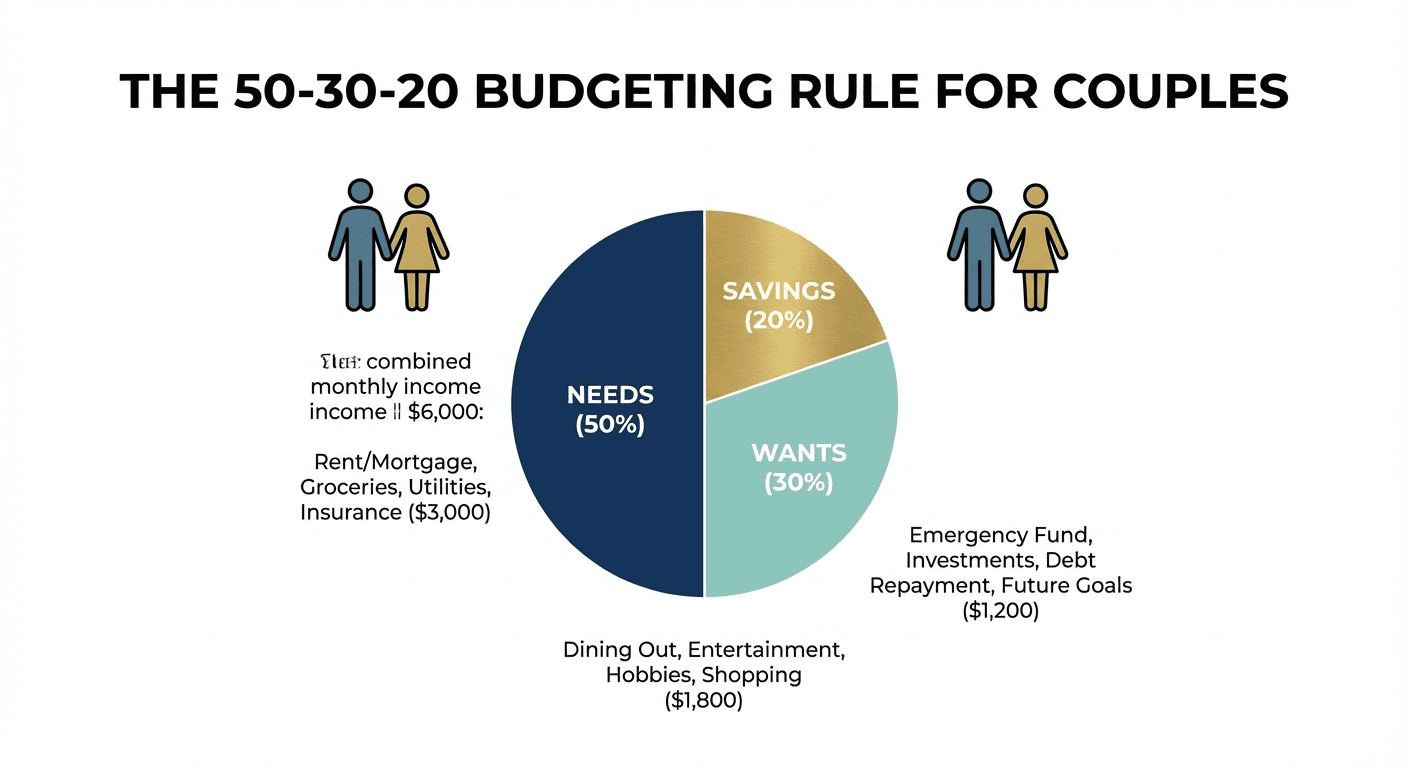

Hybrid (50/30/20 Rule)

Contribute proportionally to a shared account for needs ($3,750/mo). Keep personal accounts for wants ($2,250) and savings ($1,500).

Savings Goal Tracker

✅ On track

You need to save $1,667/month to reach your $20,000 goal in 12 months.

At your current surplus of $3,000/month, you'll reach this goal in 7 months (7mo).

How to Budget as a Couple

Managing money as a couple is one of the most important — and sometimes most challenging — aspects of a relationship. Whether you're newlyweds, engaged, or have been together for years, having a clear budget planner for couples helps you align on financial goals, avoid conflicts, and build a secure future together.

Start by having an open conversation about your incomes, debts, and financial goals. Use this couple financial planner to enter both incomes and categorise your shared expenses. The tool automatically calculates your surplus or deficit, savings rate, and provides a split recommendation based on your preferred account structure.

This joint budget calculator supports three account models: joint, separate, and hybrid. Whichever you choose, the key to managing money together is transparency and regular check-ins. Our savings goal tracker shows you exactly how long it will take to reach your next milestone at your current savings rate.

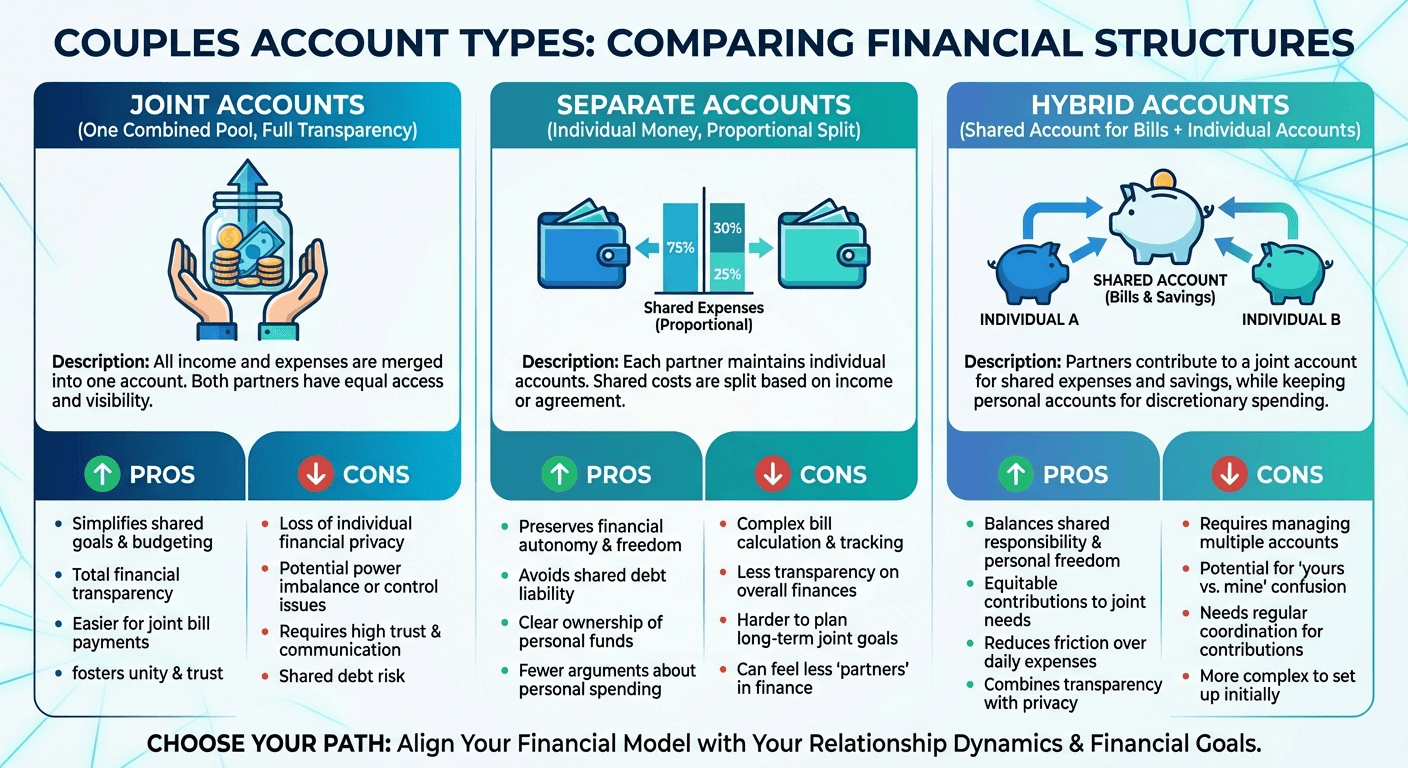

Joint vs Separate Accounts

Joint accounts work well for couples who want full transparency and simplicity. All income goes into one pot, and all expenses come out of it. This approach builds trust and makes it easy to track household finances.

Separate accounts suit couples who value financial independence. Each partner manages their own money and contributes a proportional share to shared expenses. This works especially well when there's a significant income gap.

Hybrid accounts offer the best of both worlds. Couples maintain a shared account for needs (rent, utilities, groceries) and keep individual accounts for personal spending and discretionary purchases.

The 50/30/20 Rule for Couples

The 50/30/20 rule is a simple budgeting framework that works brilliantly when you're learning how to budget as a couple. Allocate 50% of your combined after-tax income to needs (housing, utilities, groceries, insurance), 30% to wants (entertainment, dining out, hobbies, personal spending), and 20% to savings and debt repayment.

When applied to a couple's budget, the key is using combined income as the baseline. This ensures the household stays on track regardless of individual earning differences. Our hybrid mode applies this framework automatically to your inputs.

For more guidance, read our articles on how to combine finances after marriage and how to start budgeting as a couple.

How to Set Financial Goals as a Couple

One of the most powerful things you can do with a couple financial planner is set shared financial goals. Without goals, budgeting becomes a chore. With goals, it becomes a shared mission — something you're working toward together, not just a spreadsheet you fill in reluctantly once a month.

The best financial goals follow the SMART framework: Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of "we want to save more," a SMART goal is "we will save $25,000 for a house deposit by December 2027 by setting aside $800/month." The difference is night and day — the second version gives you something to track and celebrate.

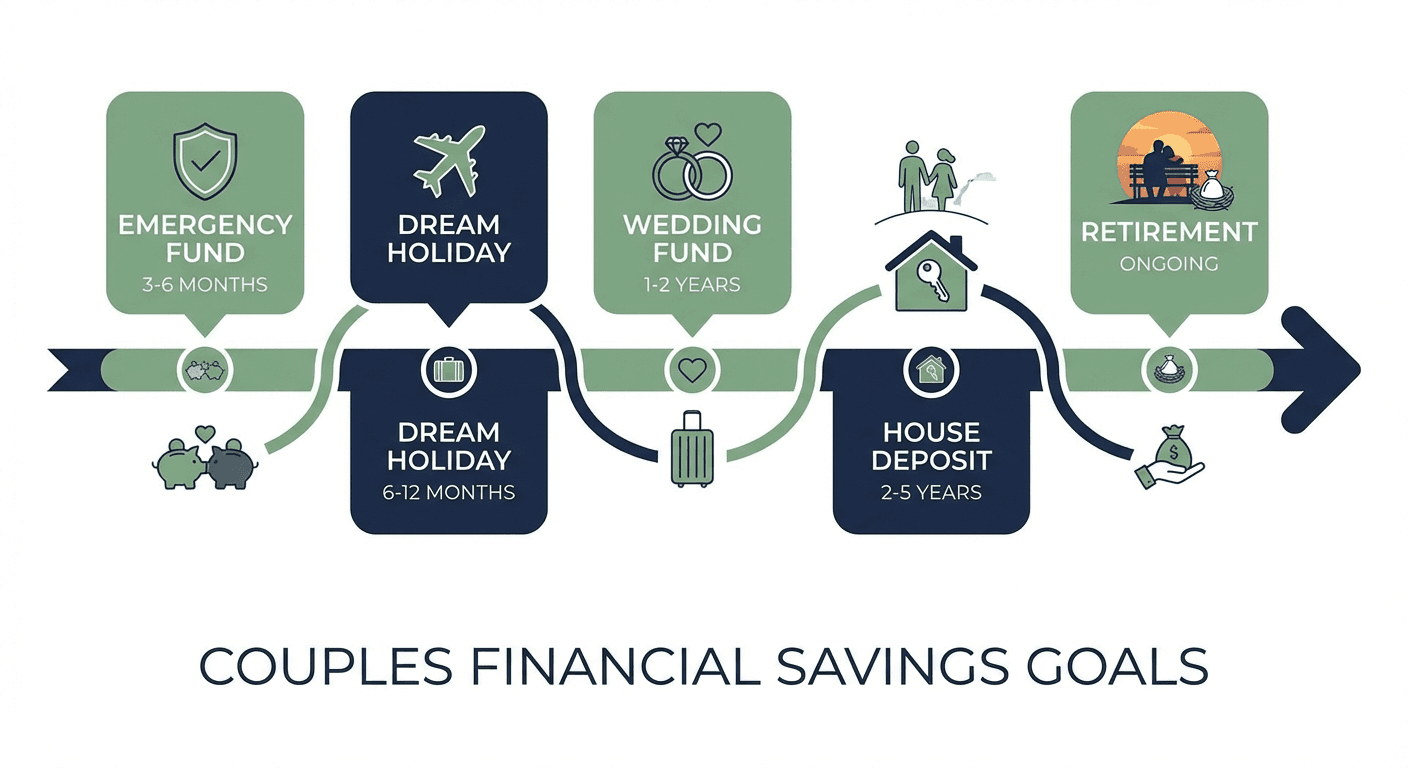

Short-Term vs Long-Term Goals

Short-term goals (0–2 years) keep you motivated. These might include a holiday, a new car, or building your emergency fund. Long-term goals (3+ years) define your future together: a home deposit, early retirement, children's education, or a business. Both matter. Neglecting short-term goals leaves the budget feeling punishing. Neglecting long-term goals leaves you financially vulnerable.

A good rule of thumb: emergency fund first. Before you save for a holiday or a car, build 3–6 months of combined living expenses in a high-interest savings account. This buffer is what keeps a financial shock (job loss, medical bill, car repair) from blowing up your entire budget. Once that's in place, you can allocate confidently toward other goals.

Use the Savings Goal Tracker above to model both short-term and long-term targets. Toggle between goals to see how adjusting your monthly savings allocation changes your timeline. If you want to reach a goal faster, look at either reducing expenses (our pie chart makes this easy to spot) or increasing income — and then re-run the numbers.

Managing money together works best when both partners have input on which goals matter most. A common exercise: each partner writes their top three financial priorities independently, then compares. You'll often find more alignment than you expected — and the gaps are worth a focused conversation.

Warning Signs in a Partner's Financial Habits

Combining finances requires trust. Before going fully joint, it's worth knowing the warning signs that a partner's financial habits could cause problems down the track.

- Secrecy about money. If your partner refuses to discuss income, debt, or spending — or gets defensive when money comes up — that's a red flag. Healthy financial partnerships require openness. A partner who hides debt or spending is creating a liability you could be sharing without knowing it.

- Impulse spending that derails plans. Everyone makes occasional unplanned purchases. But if your partner regularly spends money you've allocated to savings or bills, it signals a deeper issue with impulse control. One partner's spending patterns will directly affect a shared budget's success.

- Refusing to engage with the budget. A couple financial planner only works if both partners participate. If one partner disengages from every money conversation, avoids the budgeting tool, or dismisses the exercise as unimportant, the household has a structural problem — not a spreadsheet problem.

- Carrying high-interest debt without a plan. Some debt is unavoidable. But a partner who carries multiple maxed-out credit cards or payday loans, with no strategy to pay them down, brings significant financial risk into a shared life. Prioritise a debt repayment plan before combining finances fully.

- Drastically different risk tolerances. One partner wants to invest aggressively; the other wants every dollar in a savings account. Neither is wrong, but a large mismatch in risk tolerance can create ongoing friction. Have an explicit conversation about investment philosophy before combining finances significantly.

None of these are automatically deal-breakers — but they are conversations you need to have. A couples financial counsellor can help if these discussions feel too charged to navigate alone.

How Long to Save for Common Goals

One of the most practical uses of a joint budget calculator is modelling how long it takes to reach common savings goals. The table below shows estimated months to save at three different savings rates based on your combined income.

| Goal | Target | 10% savings rate | 15% savings rate | 20% savings rate |

|---|---|---|---|---|

| House deposit | $50,000 | 67 months | 45 months | 33 months |

| House deposit | $80,000 | 107 months | 71 months | 53 months |

| House deposit | $100,000 | 133 months | 89 months | 67 months |

| Car | $15,000 | 20 months | 13 months | 10 months |

| Car | $25,000 | 33 months | 22 months | 17 months |

| Holiday | $5,000 | 7 months | 4 months | 3 months |

| Holiday | $10,000 | 13 months | 9 months | 7 months |

| Wedding | $25,000 | 33 months | 22 months | 17 months |

| Wedding | $40,000 | 53 months | 36 months | 27 months |

Based on $7,500/month combined income. Use the Savings Goal Tracker above to calculate your exact timeline.

Money Date Night: How to Review Your Budget Together

The couples who succeed financially aren't necessarily the ones with the highest income — they're the ones who communicate about money consistently. A monthly "money date" turns budget reviews from a stressful obligation into a positive shared ritual.

Here's how to make it work:

- Set a recurring date. Last Sunday of the month, first Friday evening — whatever works. Put it in both calendars. Treat it like any other date: show up, be present, don't cancel it because you're tired or things feel awkward.

- Create a comfortable environment. Order your favourite takeaway, make coffee, sit somewhere relaxed. Money conversations go better when you're not stressed. Avoid reviewing the budget right after an argument or during a period of financial anxiety if you can help it.

- Review the numbers together — not alone. Pull up this budget planner and go through each category. Compare what you planned to spend vs what you actually spent. No blame, just data. "We went $200 over on groceries — should we adjust the budget or change our shopping habits?"

- Celebrate wins. Did you hit your savings target? Stay under budget on entertainment? Acknowledge it. Positive reinforcement makes the next month's money date feel worth showing up for.

- Adjust the plan, not the past. If something didn't work last month, change the budget going forward. Don't spend energy on guilt — spend it on a better plan. Budgets are living documents. They should evolve as your life does.

- Set one next-month goal. End every money date with a single concrete action: "Next month we're going to reduce eating out by $100" or "We're going to automate our savings transfer so it happens on pay day." Small wins compound.

The goal of a money date isn't to achieve perfection. It's to stay aligned. Couples who talk about money regularly report fewer financial arguments and higher relationship satisfaction — not because they have more money, but because they're on the same page about it.

For more guidance, read our articles on how to combine finances after marriage and how to start budgeting as a couple.

Frequently Asked Questions

Should couples have joint or separate bank accounts?

There's no single right answer. Joint accounts simplify shared expenses and build transparency. Separate accounts preserve financial independence. Many couples find a hybrid approach works best — a joint account for shared bills and individual accounts for personal spending.

What is the 50/30/20 rule for couples?

The 50/30/20 rule suggests allocating 50% of combined after-tax income to needs (rent, utilities, groceries), 30% to wants (entertainment, dining out, hobbies), and 20% to savings and debt repayment. For couples, this is applied to the combined household income.

How should couples split bills if one partner earns more?

A proportional split is often fairest. If Partner 1 earns 60% of the household income, they contribute 60% of shared expenses. This ensures both partners have a similar proportion of disposable income after bills.

How much should couples save each month?

Financial advisors recommend saving at least 20% of combined income. This includes emergency fund contributions, retirement savings, and other financial goals. Start with whatever you can and increase gradually.

How often should couples review their budget?

Review your budget together at least once a month. A monthly money date helps you track spending, adjust categories, celebrate wins, and address any financial concerns before they become problems.