Marriage & Money

How to Combine Finances After Getting Married

Learn how to combine finances after getting married with proven strategies for joint accounts, budgeting, and debt management. Start your plan today.

Combining finances after getting married is one of the most important steps newlyweds face — and one of the most overlooked. This guide walks you through proven strategies for merging accounts, creating a joint budget, managing debt together, and building shared financial goals that strengthen your marriage.

By Rachel M., Certified Financial Educator | Last updated: March 2026

Table of Contents

- Why Combining Finances Matters

- Three Approaches to Merging Money

- Step-by-Step: How to Combine Your Finances

- How to Handle Debt as a Couple

- Creating Your First Joint Budget

- Best Tools for Managing Money Together

- Setting Shared Financial Goals

- The Money Date: Regular Financial Check-Ins

- Common Mistakes Couples Make with Shared Finances

- Frequently Asked Questions

- Sources and Methodology

Why Combining Finances Matters

Money is consistently cited as one of the top sources of conflict in marriages. Research from the Institute for Divorce Financial Analysts suggests that financial disagreements are a leading contributor to divorce. The issue is rarely about how much money a couple earns — it is about how they communicate, plan, and make decisions together.

When you combine finances after getting married, you are doing more than merging bank accounts. You are building a system of shared trust. You are agreeing on priorities. You are creating a financial partnership that supports everything else in your marriage — from where you live to how you raise children to when you retire.

Couples who actively manage money together report higher relationship satisfaction. That does not mean you need to merge every dollar. It means you need a plan, clear communication, and a structure that works for both of you.

If you are newly married or engaged and feeling uncertain about where to start, you are in the right place. This guide covers every step, from the first honest conversation to the tools that make joint budgeting simple.

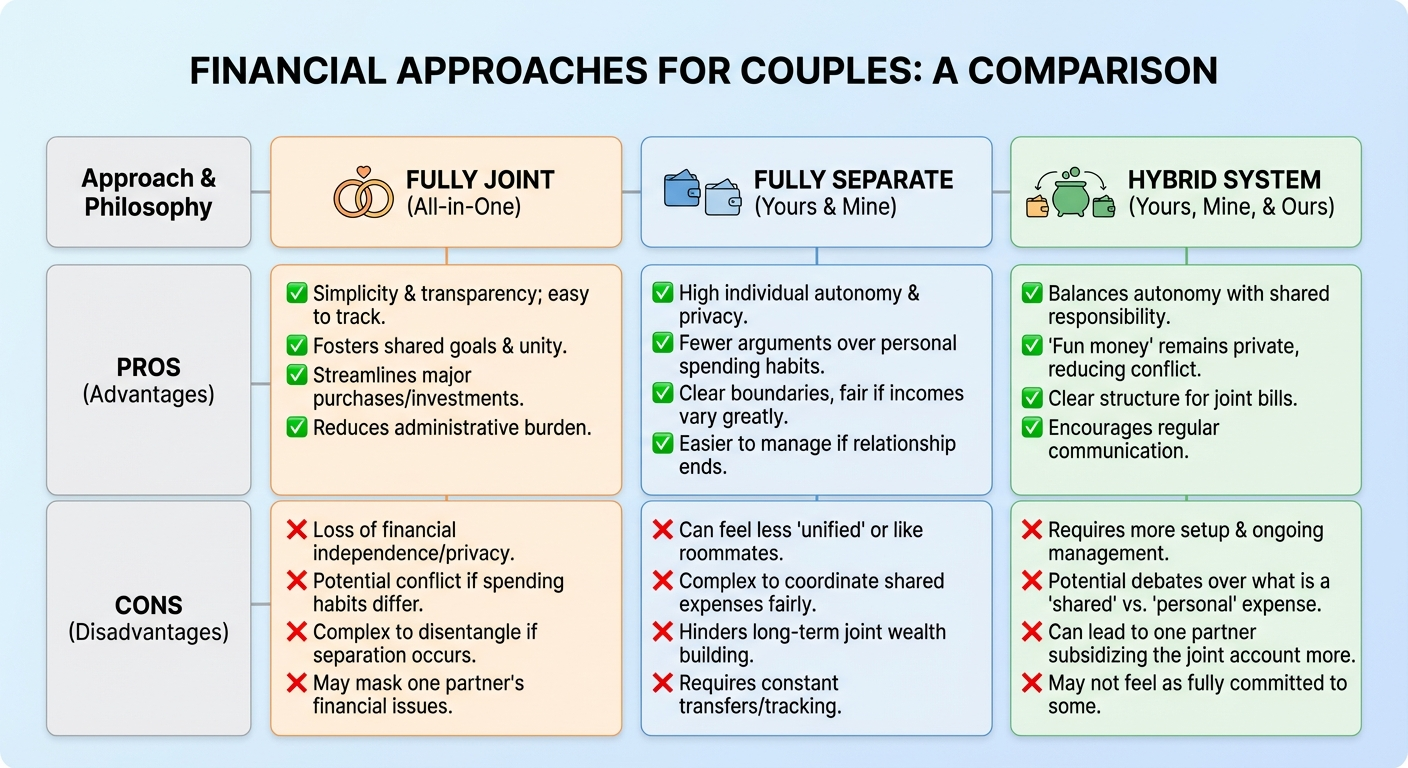

Three Approaches to Merging Money

Before you open a joint account or rework your budget, decide which financial model fits your relationship. There are three proven approaches, and none of them is universally "right."

1. Fully Combined

All income goes into a single joint account. All bills, savings, and spending come from that account. Both partners have full visibility and access.

Best for: Couples with similar spending habits, comparable incomes, and high financial trust. This approach simplifies everything but requires strong communication since every purchase is visible.

2. Fully Separate

Each partner maintains their own accounts. You split shared expenses by percentage of income or 50/50. Individual savings and spending remain independent.

Best for: Couples who value financial autonomy, have significant income differences, or are blending families with existing financial obligations. This approach requires a clear agreement on how shared expenses are divided.

3. Hybrid (The Three-Account System)

Both partners contribute to a joint account for shared expenses — mortgage, utilities, groceries, savings goals — while keeping personal accounts for individual spending. This is the most popular approach among financial planners.

Best for: Most couples. The hybrid model balances transparency with independence. Each person gets a guilt-free spending allowance while shared responsibilities are covered first.

Many couples who start with one approach shift to another over time. The key is to choose a starting point, test it for three to six months, and adjust based on what you learn.

Step-by-Step: How to Combine Your Finances

Here is a practical roadmap for merging your money. You do not need to complete all of these in a single weekend — take them in order at whatever pace feels manageable.

Step 1: Have the Full Disclosure Conversation

Before you merge anything, lay everything on the table. Both partners should share:

- Total income (salary, side income, investments)

- All debts (student loans, credit cards, car payments, personal loans)

- Credit scores (check free at annualcreditreport.com)

- Existing accounts (checking, savings, retirement, brokerage)

- Financial obligations (child support, family loans, subscriptions)

This is not about judgment. It is about building a complete picture. Many couples discover debts or accounts their partner never mentioned — not out of dishonesty, but because they never had a reason to discuss them.

Step 2: Decide on Your Account Structure

Based on the three models above, choose your approach. If you go hybrid (which most couples do), decide:

- How much each person contributes to the joint account (equal amounts or proportional to income)

- What expenses the joint account covers

- How much goes into each personal account

A common formula is the proportional contribution model. If one partner earns 60% of household income and the other earns 40%, they contribute to the joint account in that same ratio. This feels fairer than a 50/50 split when incomes differ significantly.

Step 3: Open Your Joint Accounts

You will typically need:

- A joint checking account for everyday shared expenses

- A joint savings account (or high-yield savings) for emergency fund and shared goals

- Optionally, a joint credit card for shared purchases that earns rewards

When choosing a bank, look for no monthly fees, a competitive savings rate, a strong mobile app, and easy account access for both partners. Many couples find online banks offer better rates and lower fees than traditional banks.

Step 4: Automate Your System

Once accounts are open, set up automatic transfers:

- Payday → fixed amount to joint checking

- Joint checking → automatic bill payments (rent/mortgage, utilities, insurance)

- Joint checking → joint savings (pay yourselves first)

- Remaining income → personal accounts

Automation removes the friction of manually moving money and ensures shared obligations are always covered before personal spending.

Step 5: Update Beneficiaries and Legal Documents

This step is easy to forget but critical. After marriage, update:

- Retirement account beneficiaries (401k, IRA)

- Life insurance beneficiaries

- Bank account beneficiaries

- Will and estate documents

If you are also navigating the broader logistics of post-wedding life, startweddingplanning.com has useful checklists for managing the administrative side of newlywed transitions.

How to Handle Debt as a Couple

Debt is the elephant in the room for many newlyweds. According to the Federal Reserve, the average American household carries over $100,000 in total debt including mortgages. When you marry someone, their financial situation becomes part of your shared reality.

Decide on a Debt Strategy Together

You have two main options:

Option A: Tackle all debt together. Pool resources and attack debt as a team regardless of who incurred it. This accelerates payoff but requires both partners to feel comfortable paying for the other's past decisions.

Option B: Keep debt repayment separate. Each partner handles their own pre-marriage debt from personal funds, while shared income covers shared expenses. This can feel fairer but may slow down overall debt elimination.

Many couples take a middle path — they attack high-interest credit card debt together (because the interest is damaging to both of you) while keeping lower-interest student loans with the original borrower.

Choose a Payoff Method

- Avalanche method: Pay minimums on everything, put extra money toward the highest-interest debt first. Saves the most money over time.

- Snowball method: Pay minimums on everything, put extra money toward the smallest balance first. Builds psychological momentum through quick wins.

For a deeper dive on finding the right budgeting framework for your situation, check out our guide on how to start budgeting as a couple.

Creating Your First Joint Budget

A budget is not a restriction — it is a plan for your money that reflects your shared values. Here is how to build one that actually sticks.

The 50/30/20 Framework (Adapted for Couples)

Start with a proven formula and adjust from there:

- 50% of combined take-home pay → Needs. Housing, utilities, groceries, insurance, minimum debt payments, transportation.

- 30% of combined take-home pay → Wants. Dining out, entertainment, hobbies, personal spending allowances, subscriptions.

- 20% of combined take-home pay → Savings and extra debt repayment. Emergency fund, retirement contributions, extra debt payments, sinking funds for big purchases.

Track Everything for 30 Days First

Before you set budget numbers, track where your money actually goes for a full month. Both partners should log every expense. This reveals the real spending picture — and it often surprises both people.

After 30 days, sit down together and categorize your spending. You will quickly see where you are aligned and where adjustments are needed.

Build in Personal Spending Allowances

This is non-negotiable for a healthy financial partnership. Each partner gets a set amount of money each month to spend however they want, no questions asked. It eliminates the resentment that comes from feeling monitored on every purchase.

The amount does not matter as much as the agreement. Whether it is $50 or $500 per month, having personal spending freedom within a structured budget keeps both partners happy.

For a structured template you can use together, see our monthly budget template for couples.

Best Tools for Managing Money Together

The right tools make shared finances dramatically easier. Here are the best budgeting apps and resources for couples in 2026.

| Option | Best For | Price Range | Rating |

|---|---|---|---|

| YNAB (You Need a Budget) | Couples who want hands-on budget control | $14.99/mo or $99/yr | ⭐⭐⭐⭐⭐ |

| Honeydue | Couples new to shared budgeting | Free | ⭐⭐⭐⭐½ |

| Goodbudget | Couples who prefer envelope-style budgeting | Free / $10/mo Plus | ⭐⭐⭐⭐ |

| Couples Financial Workbook | Structured offline money conversations | $10–$25 | ⭐⭐⭐⭐ |

Visual guide: Setting up a joint budgeting system with the three-account approach

YNAB (You Need a Budget)

The gold standard for zero-based budgeting. YNAB lets both partners access the same budget in real time, assign every dollar a job, and track goals together. The learning curve is worth it — couples who stick with YNAB consistently report feeling more in control of their money.

Best for: Couples who want hands-on budget control

Price: $14.99/month or $99/year

Honeydue

Built specifically for couples. Honeydue lets you see both partners' accounts in one place, set spending limits by category, and chat about finances within the app. You control what your partner can see — full balances or just shared categories.

Best for: Couples new to shared budgeting who want a simple start

Price: Free

Goodbudget

A digital version of the envelope budgeting system. Goodbudget syncs across devices so both partners work from the same set of virtual envelopes. Great for couples who want to allocate cash into categories without linking bank accounts directly.

Best for: Couples who prefer envelope-style budgeting

Price: Free basic plan; Plus plan $10/month

Couples Financial Workbook

Sometimes analog works best. A dedicated couples financial workbook lets you sit together, write out goals, track spending by hand, and build the habit of regular money conversations. Many couples use a physical workbook alongside a digital app.

Best for: Couples who want structured offline money conversations

Price: $10–$25

Setting Shared Financial Goals

A budget without goals is just expense tracking. Goals give your money purpose and give both partners something to work toward together.

Short-Term Goals (1–12 Months)

- Build an emergency fund covering three to six months of shared expenses

- Pay off high-interest credit card debt

- Save for a vacation or holiday trip

- Build a home maintenance fund

Medium-Term Goals (1–5 Years)

- Save for a house down payment

- Pay off student loans

- Start investing together

- Save for starting a family

Long-Term Goals (5+ Years)

- Maximize retirement contributions

- Build college savings for children

- Plan for financial independence

- Create a legacy or charitable giving plan

How to Prioritize Goals

You cannot fund everything at once. Use this hierarchy:

- Employer retirement match — this is free money, never leave it on the table

- Emergency fund — aim for one month of expenses first, then build to three to six months

- High-interest debt — anything above 7% interest is costing you more than investing would earn

- Medium-term goals — down payment, car fund, family planning

- Additional retirement and investing — beyond the employer match

Write your goals down together. Assign a dollar amount and a target date to each one. Review them monthly. Goals that are written, specific, and reviewed regularly are dramatically more likely to be achieved.

The Money Date: Regular Financial Check-Ins

The single best habit couples can build is a regular money date. This is a scheduled time — weekly or bi-weekly — where you sit down together and review your finances.

What to Cover in a Money Date

- Review spending against your budget categories

- Check progress toward savings goals

- Discuss upcoming expenses (car registration, gifts, medical bills)

- Flag any concerns before they become arguments

- Celebrate wins (debt milestones, savings targets hit)

How to Make Money Dates Actually Happen

- Schedule them at the same time each week — treat them like a recurring appointment

- Keep them short — 15 to 30 minutes maximum

- Make them pleasant — pair with coffee, dessert, or a glass of wine

- Stay solution-focused — this is planning time, not blame time

- Alternate who leads the conversation each week

The couples who consistently report the lowest financial stress are not the ones who earn the most. They are the ones who talk about money regularly, without shame or blame.

Common Mistakes Couples Make with Shared Finances

Avoiding the Conversation Entirely

The biggest mistake is not talking about money at all. Many couples assume they are on the same page because they have never disagreed — but that is usually because they have never discussed it. Silence is not alignment.

Going All-In Too Fast

Merging everything the day after the wedding can create unnecessary stress. Start with one joint account for shared bills. Add complexity gradually as you build confidence in your system. Our budgeting for couples guide covers how to ease into shared financial management at the right pace.

Keeping Financial Secrets

Financial infidelity — hiding purchases, secret accounts, or undisclosed debt — is more damaging than most couples realize. According to a National Endowment for Financial Education survey, financial deception affects over 40% of couples. Full transparency is the foundation.

Not Accounting for Income Differences

A 50/50 split sounds fair, but if one partner earns significantly more than the other, it creates an unequal burden. Proportional contributions based on income percentage are generally more sustainable and less resentful.

Forgetting About Taxes

Marriage changes your tax situation. File jointly in most cases to maximize deductions, but review your specific situation with a tax professional. Update your W-4 withholdings after marriage to avoid a surprise tax bill or unnecessarily large refund.

Neglecting Insurance Updates

After marriage, review health insurance (one partner's plan may be better), update auto insurance (multi-car discounts), and consider life insurance if you do not already have it. These changes can save hundreds of dollars annually.

Frequently Asked Questions

Should married couples combine all their finances?

Not necessarily. Many successful couples use a hybrid approach where they maintain a joint account for shared expenses like mortgage, utilities, and groceries while keeping separate personal accounts for individual spending. The best approach depends on your communication style, income levels, and financial goals.

When should you combine finances after getting married?

Most financial advisors recommend starting the conversation before the wedding and beginning to combine finances within the first three months of marriage. However, there is no universal deadline. The key is to have an open discussion, agree on a system, and implement it at a pace that feels comfortable for both partners.

How do you combine finances when one spouse has debt?

First, have a transparent conversation about all debts including amounts, interest rates, and minimum payments. Then decide together whether to pay off debt from joint funds or keep debt repayment separate. Many couples choose to attack high-interest debt together while keeping student loans or older debts with the original partner. Create a shared debt payoff plan with clear milestones.

What is the best joint bank account for married couples?

The best joint account depends on your priorities. Look for accounts with no monthly fees, high-yield savings options, and strong mobile banking features. Many couples prefer online banks that offer higher interest rates on savings. Compare fee structures and features before committing to a bank.

How do you budget together when you have different spending habits?

Start by tracking all spending for 30 days so both partners see where money goes. Then agree on budget categories together, giving each person a guilt-free personal spending allowance. Use a budgeting app that both partners can access in real time. Schedule weekly or bi-weekly money check-ins to review spending and adjust as needed. The goal is alignment, not control.

Should married couples have separate bank accounts?

Having separate accounts alongside a joint account is perfectly healthy. Many financial planners recommend the three-account system: one joint account for shared bills and goals, plus one personal account for each spouse. This preserves individual autonomy while ensuring shared responsibilities are covered.

Sources and Methodology

This article draws on the following sources and professional guidance:

-

Institute for Divorce Financial Analysts (IDFA) — Survey data on financial factors contributing to divorce, referenced for the relationship between money conflict and marital outcomes.

-

Federal Reserve Survey of Consumer Finances — Data on average household debt levels in the United States, used to contextualize debt management strategies for married couples.

-

National Endowment for Financial Education (NEFE) — Research on financial infidelity prevalence among couples, cited in the common mistakes section regarding financial transparency.

All strategies and recommendations in this guide are based on widely accepted personal finance principles including the 50/30/20 budgeting framework, the debt avalanche and snowball methods, and the three-account system recommended by certified financial planners. Specific product recommendations are based on feature comparison and suitability for couples — no tool or service paid for inclusion in this article.

Have questions about combining finances with your partner? Start with the conversation — that is always the hardest and most important step. For more guides on building a financial plan together, explore budgetingforcouples.com.