Couples Budgeting

Emergency Fund Goals for Couples: How Much to Save in 2026

Discover the ideal emergency fund for couples in 2026. Learn how much to save, where to keep it, and strategies to build one together without stress.

Most financial advisors recommend couples keep 3-6 months of essential expenses in an easily accessible savings account. That means if your household spends $4,500 per month on essentials, your target emergency fund range is $13,500 to $27,000. The exact number within that range depends on your income stability, health, dependants, and debt obligations — and getting it right could save your family's financial future.

Table of Contents

- Why Couples Need a Dedicated Emergency Fund

- How Much Should Couples Save? The 3-6 Month Guideline

- Emergency Fund Tiers: Starter, Transition, and Full Fund

- Factors That Change Your Target Amount

- Where to Keep Your Couple's Emergency Fund

- Building Your Emergency Fund Together: Strategies That Work

- Common Mistakes Couples Make with Emergency Savings

- Emergency Fund vs. Other Financial Priorities

- Frequently Asked Questions

- Sources & Methodology

Why Couples Need a Dedicated Emergency Fund

Money conflicts are one of the leading causes of relationship strain, and most of those conflicts trace back to a lack of financial buffer. When an unexpected car repair, medical bill, or job loss hits a couple with no emergency savings, the stress doesn't just affect their bank account — it seeps into every conversation, every decision, and every aspect of their partnership.

An emergency fund is fundamentally different from regular savings. It's not for vacations, new furniture, or the occasional splurge. It's specifically designed to catch you when life goes sideways — and life always goes sideways at some point. The Federal Reserve's 2023 Survey of Consumer Finances found that 37% of adults could not cover a $400 emergency without borrowing money or selling something. Couples with children, variable incomes, or existing debt are even more vulnerable.

For couples specifically, an emergency fund serves an additional purpose: it protects both partners. If one person loses their job, the emergency fund covers essential expenses while they search for new work. Without it, the earning partner faces enormous pressure to accept the first offer that comes along — regardless of whether it's the right fit — simply because the bills are due.

Financial stress takes a real toll on relationships. A 2021 study published in the Journal of Family Psychology found that couples who argued about money at least once a week were 30% more likely to separate than couples who disagreed about finances rarely or never. Building a robust emergency fund doesn't just protect your finances — it protects your relationship too.

[INTERNAL LINK: How to Build a Joint Budget as a Couple -> /how-to-build-a-joint-budget] [INTERNAL LINK: Couples Guide to Managing Debt Together -> /couples-guide-managing-debt]

How Much Should Couples Save? The 3-6 Month Guideline

The standard recommendation is to save 3-6 months of essential expenses. But what does "essential expenses" actually mean? This is where many couples go wrong — they calculate based on their gross income when they should be looking at what they truly need to survive.

Calculating Your Essential Monthly Expenses

Essential expenses include:

- Housing costs: Rent or mortgage, property taxes, home insurance

- Utilities: Electricity, gas, water, internet, phone

- Food: Groceries and household essentials (not dining out)

- Transportation: Car payment, insurance, fuel, public transit

- Healthcare: Health insurance premiums, prescriptions, medical appointments

- Debt minimums: Minimum payments on student loans, car loans, credit cards

- Childcare: If applicable, the non-negotiable childcare costs

- Pet care: Food and routine veterinary for family pets

What does NOT count as essential: dining out, subscriptions, entertainment, gym memberships, travel, clothing beyond basic replacement, and discretionary spending.

Once you've calculated your monthly essential total, multiply by 3 for a baseline target and by 6 for a full security target. A couple spending $4,000/month in essentials should aim for $12,000 minimum, with $24,000 as the full target.

Emergency Fund Target Summary

| Household Monthly Essentials | Minimum Target (3 Months) | Full Target (6 Months) |

|---|---|---|

| $3,000 | $9,000 | $18,000 |

| $4,000 | $12,000 | $24,000 |

| $5,000 | $15,000 | $30,000 |

| $6,000 | $18,000 | $36,000 |

| $7,500 | $22,500 | $45,000 |

Based on 2026 cost-of-living averages. Adjust for your specific city and lifestyle.

[INTERNAL LINK: Calculating Your Couple's Emergency Fund Target -> /calculating-emergency-fund-target]

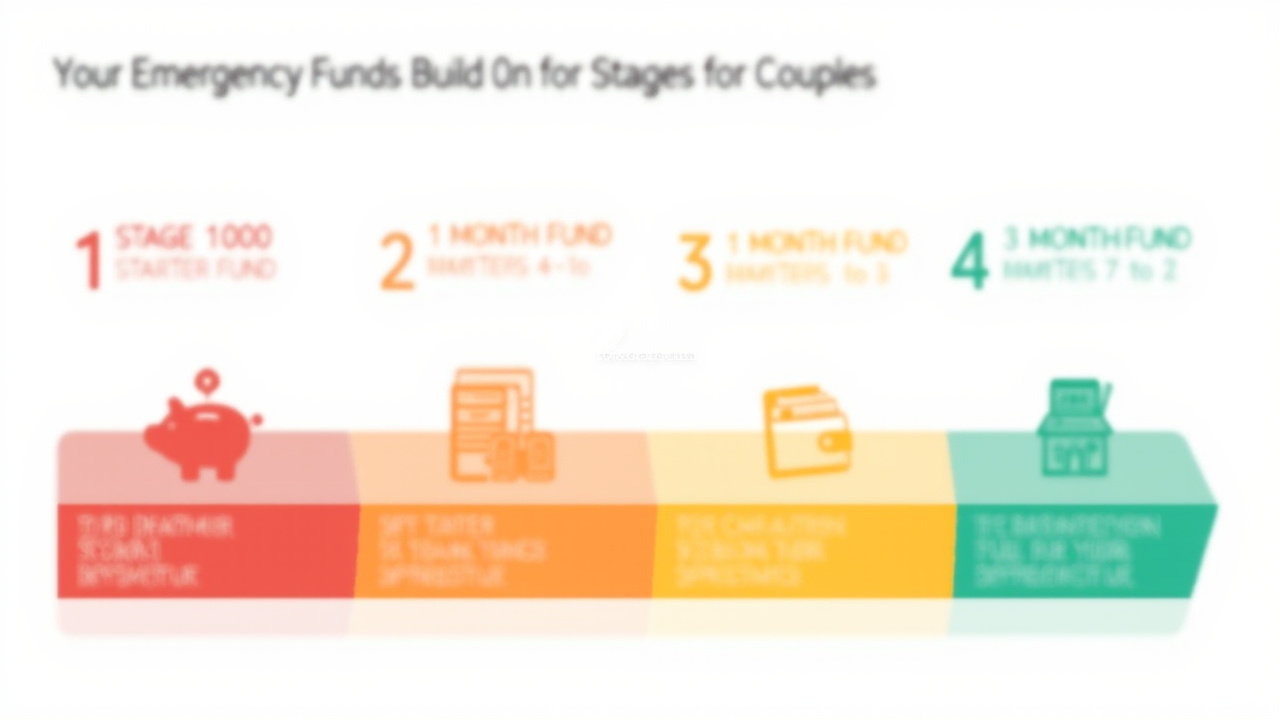

Emergency Fund Tiers: Starter, Transition, and Full Fund

Not every couple starts at zero and builds to $30,000 overnight. Financial planners typically recommend a tiered approach that gives you protection at every stage while you work toward your full target.

Tier 1: Starter Emergency Fund ($1,000-$2,000)

Before you tackle debt, build this small buffer. It won't cover a job loss, but it will prevent a flat tyre or emergency room visit from sending you back to credit cards. This amount should be accessible within 24 hours — a standard savings account, not invested anywhere.

Tier 2: Transition Emergency Fund (1-3 months of essentials)

Once your starter fund is complete, expand it to cover at least one month of essential expenses. This is your transition zone — enough to handle a job loss or major home repair without panic. Aim for this tier before accelerating debt payoff beyond minimum payments.

Tier 3: Full Emergency Fund (3-6 months of essentials)

This is the finish line. Three months is the baseline for dual-income households with stable jobs. Six months is recommended for single-income households, self-employed individuals, anyone in a commission-based role, or families with significant health concerns.

[INTERNAL LINK: The Couple's Financial Priority Order: What to Save For First -> /financial-priority-order-couples]

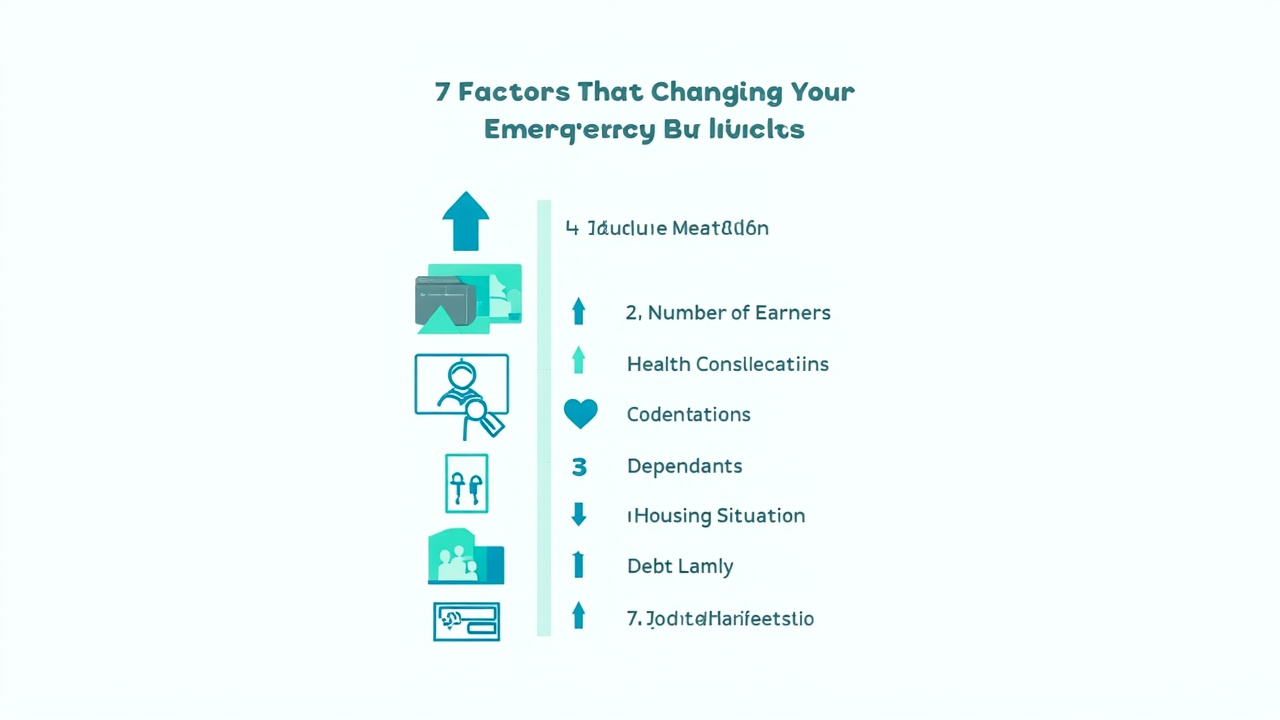

Factors That Change Your Target Amount

The 3-6 month guideline is a starting point. Several factors should push you toward the higher end of that range — or even beyond it.

Income Stability

If both partners have stable salaried jobs with in-demand skills, 3 months may be sufficient. If either partner works in a volatile industry, relies on commissions, or has seasonal income, lean toward 6 months or more. Freelancers and self-employed couples should target 6-12 months — your income can disappear virtually overnight when a major client leaves.

Number of Earners

Dual-income couples have a natural buffer: if one person loses their job, the other still brings in a pay cheque. Single-income households (whether by choice or circumstance) have no such protection and should lean toward the higher end of the range.

Health Considerations

If either partner or a dependent has ongoing medical needs, build a larger fund. Medical emergencies often come with significant out-of-pocket costs even with good insurance. A family member with a chronic condition may also face employment discrimination during health crises, making income loss more likely.

Dependants

Children dramatically change the math. A couple with young children faces childcare costs that don't disappear just because a parent lost a job. If a single-income situation suddenly becomes the reality, emergency fund needs can spike to cover the gap in childcare, health insurance, and daily needs.

Housing Situation

Homeowners face emergency costs that renters don't: roof repairs, HVAC replacement, plumbing emergencies. If you own your home, consider adding an extra 1-2 months of expenses specifically for home emergencies on top of your baseline target.

Debt Load

Couples carrying high-interest consumer debt (credit cards, personal loans) face a harder choice during financial crises: pay the debt or cover the emergency. A larger emergency fund gives you more flexibility to weather a storm without derailing your debt payoff progress.

Job Marketability

If both partners have skills that are in high demand and can find new work quickly, you can be more aggressive with a shorter fund. If either partner would need months to find comparable work (specialised roles, career changes, geographic limitations), extend your timeline accordingly.

Where to Keep Your Couple's Emergency Fund

Location matters almost as much as amount. An emergency fund that earns 0.5% APY in a traditional bank will lose purchasing power to inflation over time. One that earns 4.5%+ in a high-yield savings account will grow while it sits waiting for an emergency.

High-Yield Savings Accounts (Best Choice)

Online banks consistently offer the highest rates because they have lower overhead than branch-based banks. As of mid-2026, several reputable online banks offer APYs above 4.5%:

- Marcus by Goldman Sachs: Competitive rates, no fees, FDIC insured

- Ally Bank: 24/7 customer service, easy-to-use interface, strong reputation

- Discover Bank: Often tops rate comparisons, no minimum balance, FDIC insured

- SoFi: Growing platform with competitive rates and additional financial products

The key features to look for: FDIC insurance (covers up to $250,000 per depositor), no monthly fees, no minimum balance requirements, and Federal Deposit Insurance Corporation coverage.

Money Market Accounts

Money market accounts typically offer slightly higher rates than savings accounts and come with check-writing privileges, which can be convenient during an emergency. However, they often have higher minimum balance requirements. If you can maintain the minimum, they're worth considering.

What NOT to Do With Emergency Funds

- Do not invest your emergency fund in stocks, bonds, or mutual funds. The whole point is liquidity — you need this money within days, not weeks. A market crash often coincides with economic recessions, which means job losses. You do not want to be forced to sell investments at a loss.

- Do not keep it in a certificate of deposit (CD) unless you can easily break it without penalty. Early withdrawal penalties eat into your returns.

- Do not keep it in your regular checking account. You want it separated so you're not tempted to use it for non-emergencies.

- Do not lend it to family. Your emergency fund is for your household's emergencies, not extended family's financial problems.

[INTERNAL LINK: Best High-Yield Savings Accounts for Couples in 2026 -> /best-high-yield-savings-accounts-couples]

Building Your Emergency Fund Together: Strategies That Work

Building a substantial emergency fund requires consistency, and consistency requires systems. Here are the strategies that actually work for couples.

Strategy 1: Automate Before You Budget

Set up an automatic transfer from your joint checking to your emergency fund savings account on the same day each month — ideally the day after payday. Money that moves automatically leaves less room for "we'll save what's left over" which never works. Treat your emergency fund contribution like a bill that must be paid.

Strategy 2: Direct Windfalls to the Fund

Tax refunds, work bonuses, monetary gifts, and unexpected income should go directly to your emergency fund — not into your checking account where it mysteriously vanishes. Agree in advance that 100% of windfalls go to the emergency fund until it's fully funded.

Strategy 3: Find Savings as a Couple

Rather than cutting one person's spending, work together to find household savings that can be redirected to emergency savings. Canceling unused subscriptions, switching to a cheaper phone plan, or reducing grocery waste by planning meals — these savings add up faster than you'd expect and rarely require difficult tradeoffs.

For couples who want a structured framework to find and redirect savings, the approach works best when both partners have input. Sitting down together monthly to review where money went — rather than assigning blame — builds the collaborative habit that makes financial progress sustainable long-term.

Strategy 4: Use the Sinking Fund Method

Rather than saving for one big emergency fund, create a "family security" sinking fund that you contribute to monthly. Over time, this builds into your full emergency fund without the overwhelm of saving $20,000+ all at once.

Strategy 5: Separate Accounts for Shared Goals

Many financial experts recommend a hybrid approach: a joint account for shared expenses and emergency fund, plus individual accounts for personal spending money. This reduces money conflicts while ensuring both partners have skin in the game on shared goals.

Strategy 6: Set Milestone Celebrations

Small wins matter. Celebrate when you hit $5,000, then $10,000, then $15,000. A simple dinner out or a nice bottle of wine rewards the behavior that got you there and reinforces the habit. Without celebration, the process feels endless and grind-y.

[INTERNAL LINK: How Couples Can Save $500+ Monthly Together -> /how-couples-save-500-monthly]

Common Mistakes Couples Make with Emergency Savings

Mistake 1: Starting Too Ambitious

Trying to save $2,000/month when you've never saved $100/month consistently is a recipe for failure. Start with what you can actually sustain — even $200/month is progress. Build the habit first, then accelerate.

Mistake 2: Treating the Emergency Fund Like a Slush Fund

Every unexpected expense is not an emergency. A new pair of shoes on sale is not an emergency. A weekend getaway that "we need right now" is not an emergency. Define what counts as a true emergency before you build the fund, and hold each other accountable to that definition.

Mistake 3: Not Telling Each Other Where the Money Is

If one partner dies or becomes incapacitated, the other needs to know about the emergency fund. Keep records, share access information, and discuss the fund as a couple on a regular basis.

Mistake 4: Paying Off Debt Before Building Any Buffer

As mentioned earlier, having zero emergency fund while paying off debt means any unexpected expense goes back on the credit cards. Build your $1,000 starter fund first, then attack debt with the remaining cash flow.

Mistake 5: Not Adjusting the Target When Life Changes

A job promotion, new baby, home purchase, or health diagnosis should trigger a reassessment of your emergency fund target. Make it a standing item in your annual financial review — at minimum — and after any major life event.

Emergency Fund vs. Other Financial Priorities

One of the most common questions couples ask is: what should we prioritise first? The order isn't always obvious.

Priority Order for Couples

- Starter emergency fund ($1,000-$2,000) — Before debt, before investing

- Employer 401(k) match — If your employer offers matching contributions, capture this immediately. It's free money.

- Credit card and high-interest debt — Pay minimums on all debts, then throw everything at the highest-interest debt first

- Full emergency fund (3-6 months) — Complete this before investing beyond the 401(k) match

- Retirement savings — Max out tax-advantaged accounts (401k, IRA)

- Other goals — College savings, major purchases, travel funds

This order assumes you're not in extreme debt (defined as credit card rates above 20% and total consumer debt exceeding one year's income). In extreme cases, consult a financial advisor or nonprofit credit counselor.

When to Pause Emergency Fund Building

There are situations where it makes sense to pause emergency fund contributions:

- If you have a 0% balance transfer card that will expire soon, directing extra cash to pay it off before the promotional rate ends may make more sense

- If you're about to face a major known expense (wedding, surgery, relocation), complete that expense first

- If one partner is about to go on unpaid leave (maternity/paternity leave, medical leave), build up before the income gap

Financial planning doesn't exist in isolation. Just as building an emergency fund protects your present, planning for retirement protects your future. For couples navigating both simultaneously, the key is to sequence strategically — not to do everything at once.

If you and your partner are also managing other lifestyle expenses that feel disconnected from your financial goals, it can help to take a broader view of where money is going each month. Many couples find that tracking every category together — including lifestyle spending — reveals savings opportunities they hadn't noticed before. Explore a couples budgeting approach on homecoffeespot.com for inspiration on tracking every dollar together

[INTERNAL LINK: Debt Payoff vs. Emergency Fund: What Should Couples Prioritize? -> /debt-payoff-vs-emergency-fund]

Frequently Asked Questions

How much should a couple have in emergency savings?

Most financial experts recommend couples aim for 3-6 months of essential expenses. This means if your household spends $4,000 per month on essentials, your target emergency fund should be between $12,000 and $24,000. The right amount depends on your income stability, health, dependants, and debt load.

Should both partners have separate emergency funds?

Financial advisors generally recommend one joint emergency fund rather than separate accounts. A joint fund ensures either partner can access money during a crisis, regardless of whose income is affected. However, some couples prefer a hybrid approach with a shared high-yield account for true emergencies and small individual accounts for personal discretionary spending.

Where is the best place to keep an emergency fund?

The best place for an emergency fund is a high-yield savings account that is separate from your daily checking account. Look for accounts offering 4.5%+ APY with no monthly fees and FDIC insurance. Popular options include Marcus by Goldman Sachs, Ally Bank, and Discover Bank. Avoid keeping emergency money in investments, as market downturns often coincide with job losses.

How long does it take to build a full emergency fund as a couple?

Building a full emergency fund typically takes 12-36 months depending on your income and savings rate. Aggressive savers can build a 6-month fund in 12-18 months by directing 20-30% of their combined income to savings. Slow builders may take 2-3 years with more modest contributions. The key is consistency — automate your savings so it happens before you can spend it.

What counts as a legitimate emergency to use emergency fund money on?

A true emergency is an unexpected, necessary expense you cannot cover with your regular budget. Legitimate uses include: job loss, medical emergencies, major home repairs (broken HVAC, plumbing), essential car repairs, and family emergencies requiring travel. Not emergencies: vacations, new furniture, routine car maintenance, holiday gifts, or elective medical procedures.

Does debt repayment take priority over building an emergency fund?

Financial experts recommend building a starter emergency fund of $1,000-$2,000 before aggressively paying debt. Without any buffer, an unexpected expense forces you back into debt or creates a financial crisis. Once you have that mini fund established, you can simultaneously build your full emergency fund while making minimum debt payments. After the emergency fund is complete, shift focus to debt payoff.

How do couples handle emergency fund contributions when incomes are very different?

When one partner earns significantly more, contribute to the emergency fund proportionally to income. For example, if one partner earns 70% of household income, they contribute 70% of the emergency fund target. Some couples prefer equal dollar contributions regardless of income, which can feel fairer to both partners. Discuss your approach openly and document your agreement in your shared financial plan.

Sources & Methodology

- Federal Reserve Board — Survey of Consumer Finances 2023. "How much could you cover if faced with an unexpected $400 expense?" Federal Reserve.gov. https://www.federalreserve.gov/

- Consumer Financial Protection Bureau (CFPB) — Emergency Fund Guidelines and Financial Literacy Resources. https://www.consumerfinance.gov/

- Federal Deposit Insurance Corporation (FDIC) — Deposit Insurance Coverage Guidelines for Joint Accounts. https://www.fdic.gov/

- U.S. News & World Report — "Best High-Yield Savings Accounts of 2026." Reviewed and updated quarterly. https://money.usnews.com/

- CNBC — "How to Build an Emergency Fund: A Step-by-Step Guide." 2026 edition. https://www.cnbc.com/

Last updated: June 2026. Interest rates and account features subject to change. Always verify current rates directly with financial institutions before opening an account.

Sarah Mitchell is a Certified Public Accountant (CPA) and personal finance coach who specialises in helping couples navigate joint financial decisions. With over a decade of experience advising households on budgeting, debt management, and wealth building, Sarah brings a practical, judgment-free approach to topics that couples often find stressful to discuss. She has helped hundreds of couples build their first emergency funds, pay off significant debt, and establish shared financial systems that actually stick. Sarah is based in Melbourne, Australia, and writes for Budgeting for Couples.