Guide

Joint Bank Account vs Separate: What Works Best for Couples

Joint bank account vs separate: the honest comparison for couples in 2026. Pros, cons, the hybrid approach, and a clear framework for deciding which setup works for your relationship.

Disclosure: Budgeting for Couples may earn commissions from qualifying purchases. This does not influence our recommendations.

By Emma Walsh, Certified Financial Planner · Last updated March 2026

For most couples, the hybrid approach works best: one joint account for shared expenses (rent, groceries, utilities) and separate individual accounts for personal spending. This creates transparency about shared finances while preserving autonomy. Fully joint accounts work when spending styles align closely. Fully separate accounts work when financial independence is a priority. There is no universally "correct" answer — the right structure depends on your relationship, income ratio, and financial goals.

The Three Main Approaches

Before diving into the details of each approach, it helps to see the three primary options side by side. Every couple's financial arrangement falls into one of these categories — or somewhere along the spectrum between them.

🏦 Fully Joint

All income goes into shared accounts. All spending comes from shared accounts.

Best for: Similar spending styles, strong financial trust, same income levels

💳 Fully Separate

Each person keeps their own accounts. Shared expenses are split and reimbursed.

Best for: Financial independence priority, very different incomes, unmarried couples

⚖️ Hybrid (Recommended)

Joint account for shared expenses + individual accounts for personal spending.

Best for: Most couples — balances transparency with autonomy

If you are already budgeting together, you may find that the 50/30/20 budget rule adapted for couples provides a useful starting framework regardless of which account structure you choose.

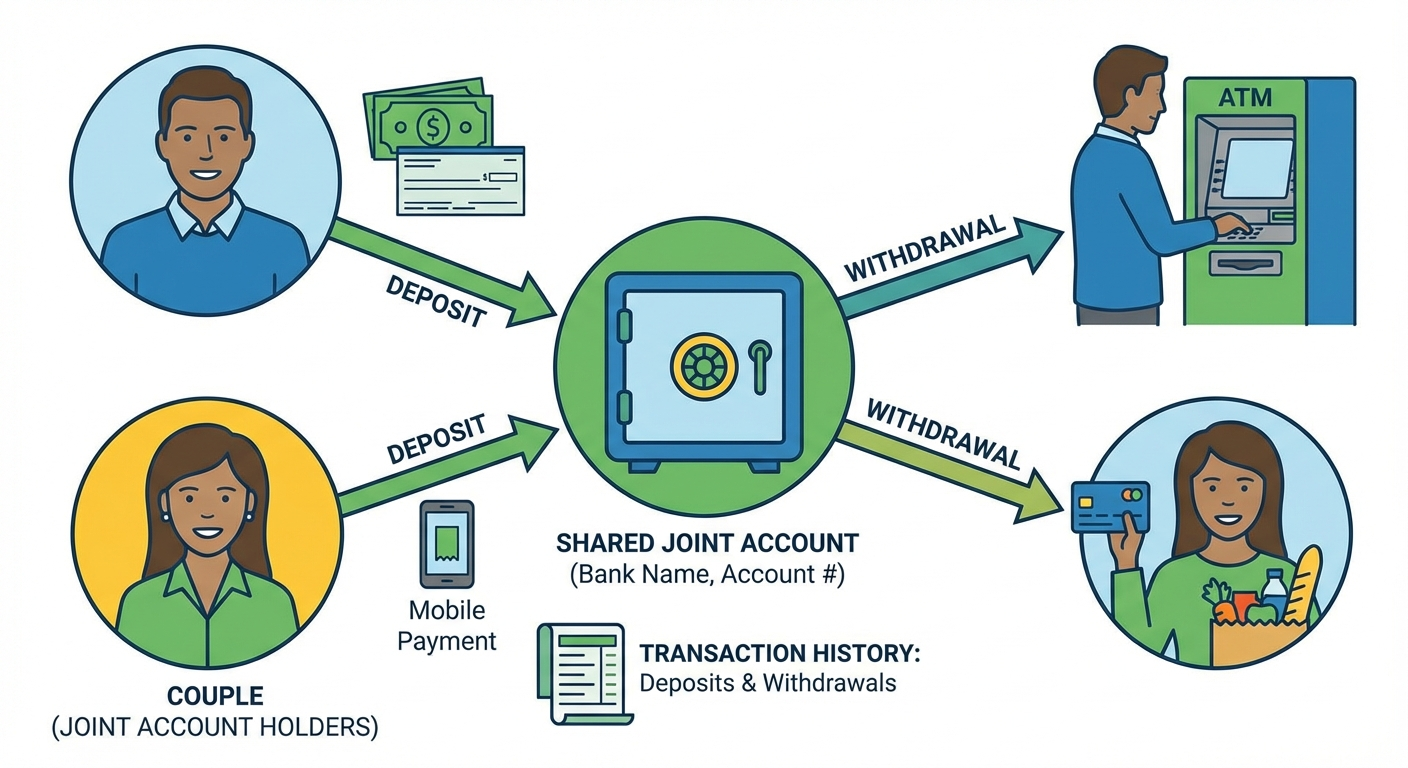

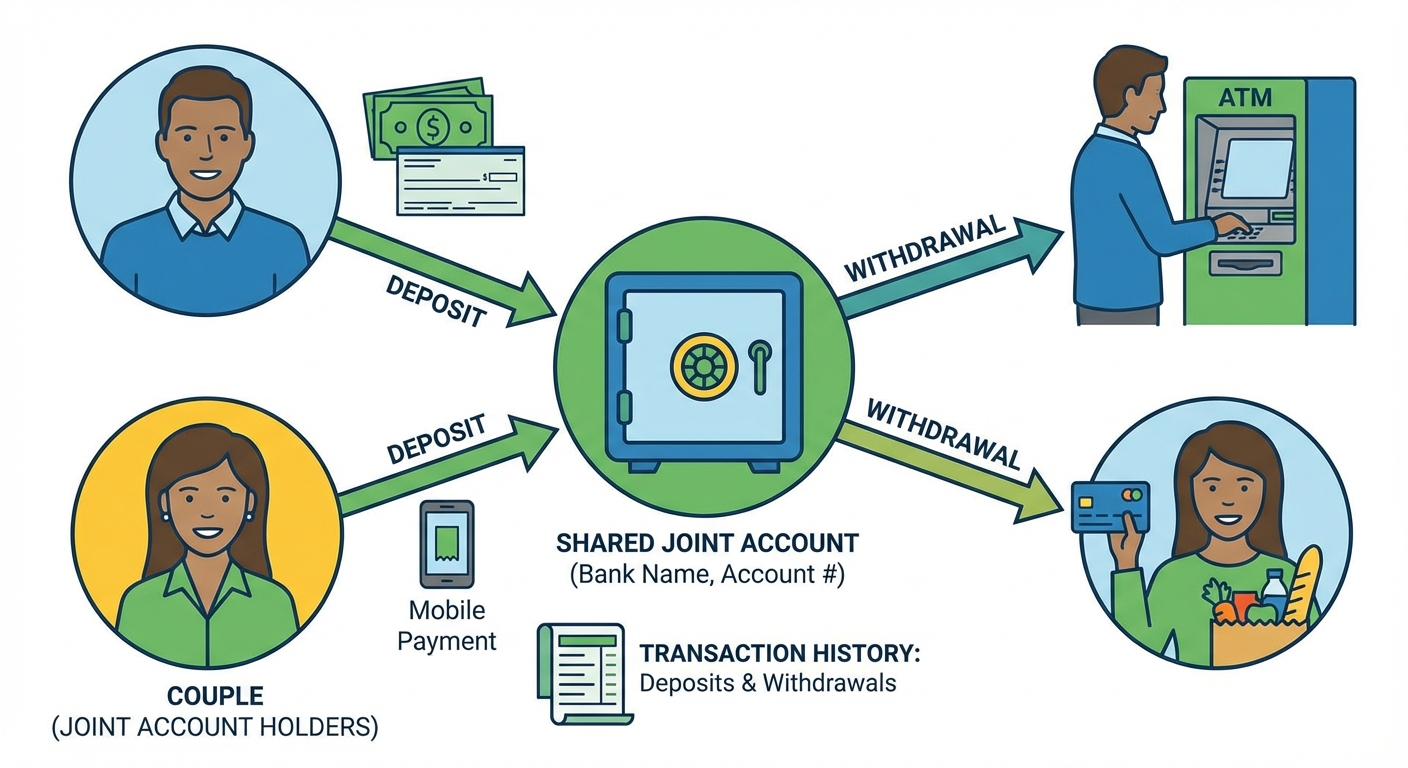

Joint Accounts: Pros and Cons

Advantages of Fully Joint Accounts

Transparency and trust: When all money flows through shared accounts, financial transparency is automatic. No questions about where money went. No hidden spending. This simplicity reduces financial conflict for couples who are already aligned on spending values.

Simplified logistics: One account to manage, one budget to track, one set of bills to pay. No spreadsheets splitting expenses. No Venmo requests for the grocery bill. For couples who find admin tasks stressful, this simplicity is a genuine relationship benefit.

Emergency coverage: Either partner can access funds immediately in an emergency, without needing to coordinate account transfers. If one partner is hospitalized or traveling, the other can handle any expense without delay.

Natural savings alignment: Saving for shared goals (house, vacation, retirement) is simpler when all savings flow to the same place. You can see your combined progress in a single view rather than adding up two separate balances.

Banking relationship benefits: Larger combined account balances may qualify for better interest rates, reduced fees, or premium banking services. Some banks waive monthly maintenance fees above certain balance thresholds.

Disadvantages of Fully Joint Accounts

Loss of financial autonomy: Every purchase is visible and potentially subject to discussion. Buying a birthday present for your partner requires coordination. Impulse purchases — even small ones — can feel like they require justification.

Conflict when spending styles differ: If one partner is a natural saver and the other a natural spender, fully joint accounts surface this tension constantly. Every transaction becomes potential friction, which is why understanding how to budget when partners have different spending habits is critical before merging accounts completely.

Vulnerability in relationship breakdown: Either party can withdraw all funds at any time. Fully joint accounts with large balances carry significant risk if the relationship ends unexpectedly.

Personal money guilt: Some people feel guilty spending on personal interests when all money is "ours." This creates unhealthy financial dynamics where one or both partners suppress their needs rather than have difficult conversations about discretionary spending.

Separate Accounts: Pros and Cons

Advantages of Fully Separate Accounts

Complete autonomy: No one monitors your spending. Personal purchases are genuinely personal. This matters especially when incomes are unequal — the lower earner doesn't feel "watched" and the higher earner doesn't feel like they need to justify personal purchases.

Financial independence resilience: If the relationship ends, each person already has their own financial infrastructure. There are no messy account splits, no frozen funds, and recovery is faster both practically and emotionally.

Fair for similar-income couples: When both partners earn similar amounts, 50/50 expense splitting with separate accounts is clean and simple. Each person pays their half and manages their remaining money independently.

Privacy for personal goals: Individual accounts allow each partner to save for personal milestones — career development courses, gifts, personal investments — without needing to justify or explain every allocation.

Disadvantages of Fully Separate Accounts

Administrative burden: Tracking who paid what, splitting grocery bills, calculating each person's share of rent. This ongoing friction can itself become a source of conflict, especially when one partner is more meticulous about tracking than the other.

Misaligned savings: Building a down payment when savings are in different accounts and managed independently creates coordination friction. One partner might be saving aggressively while the other is falling behind, and neither realizes the gap until months later.

Income inequality stress: If one partner earns significantly more than the other, strict 50/50 splitting leaves the lower earner financially stressed while the higher earner has excess discretionary income. This imbalance erodes the sense of partnership over time.

"Yours vs mine" psychology: Fully separate finances can inadvertently create a less committed "roommate" dynamic rather than a partnership. Research suggests this psychological framing can subtly undermine relationship satisfaction, even when the practical arrangement works fine.

The Hybrid Approach: Best of Both Worlds

The hybrid approach resolves most of the disadvantages of both extreme options. It is the most popular choice among millennial and Gen Z couples, and the approach most financial planners recommend as a starting point.

The System

One joint account receives contributions from both partners every month. This account pays:

- Rent/mortgage

- Shared utilities

- Groceries

- Joint savings (house, vacation, emergency fund)

- Shared subscriptions and entertainment

- Date nights and shared dining out

Individual accounts receive the remainder of each person's income after contributing to the joint account. These accounts pay for:

- Personal clothing and grooming

- Individual subscriptions and hobbies

- Personal savings and investing

- Gifts (including gifts for the partner)

- Personal dining with friends

- Any spending that doesn't affect the household

How Much to Contribute to the Joint Account

| Income Ratio | Contribution Method | Example |

|---|---|---|

| Equal incomes | 50/50 equal contribution | Both contribute $2,500/month |

| Unequal incomes (up to 2:1) | Proportional contribution | $80K earner contributes 67%, $40K earner contributes 33% |

| Very unequal incomes (3:1+) | Flat percentage of individual income | Each contributes 50-60% of personal income |

The "Personal Spending" Allowance

Both partners receive the same personal spending allowance regardless of income. This preserves equality in personal autonomy — neither partner has to ask permission for personal purchases.

For a practical example: combined household income of $120,000 after tax. Joint expenses total $5,000/month. Each partner receives $500/month personal spending. The remaining $4,000/month goes to savings and joint goals.

Automating the Hybrid System

The key to making the hybrid approach work long-term is automation. Set up automatic transfers from each paycheck so money flows into the joint account and personal accounts without either partner needing to remember to do it manually. Most banks allow you to split direct deposits, or you can set up recurring transfers on payday. Use a couples budget planner to map out your specific numbers before setting up the automation.

How to Split Expenses by Income Level

| Couple Income Split | Recommended Approach | Joint Contribution Method |

|---|---|---|

| Equal (within 20%) | 50/50 or hybrid | Each contributes the same dollar amount |

| 60/40 split | Proportional hybrid | Higher earner pays 60% of joint expenses |

| 70/30 split | Proportional hybrid | Higher earner pays 70% of joint expenses |

| 80/20+ split | Needs-based | Higher earner funds shared expenses; both get equal personal allowance |

| One partner not working | Fully joint or funded personal | The working partner funds both; agree on personal spending amounts |

The "allowance" solution for income inequality: Give both partners an equal "personal spending" allocation regardless of income. This prevents the lower earner from feeling financially controlled while acknowledging the income reality.

How to calculate your proportional split: Add both incomes together. Divide each person's income by the total. That percentage is what each person contributes to joint expenses. For example, if Partner A earns $70,000 and Partner B earns $30,000, the total is $100,000. Partner A contributes 70% of joint expenses, Partner B contributes 30%. If shared monthly expenses total $4,000, Partner A pays $2,800 and Partner B pays $1,200.

What Research Says About Money and Relationships

Key findings from academic research on couples and money:

-

Journal of Personality and Social Psychology (2018): Couples who pool finances report higher relationship satisfaction and feel more "integrated" as a unit. But this correlation is mediated by financial communication — pooling alone doesn't create satisfaction.

-

Northwestern University (2023): Couples with joint accounts reported higher daily happiness and lower financial anxiety than those with separate accounts, even after controlling for income.

-

American Psychological Association survey: Financial disagreements are cited as the #1 cause of relationship conflict and a major predictor of divorce. Account structure matters less than having regular, non-defensive money conversations.

-

National Endowment for Financial Education (2023): 43% of adults who combine finances with a partner admit to some form of financial deception. This underscores why transparency mechanisms — regular money dates, shared budget apps, open account access — matter regardless of which structure you choose.

The bottom line: There's weak evidence that fully joint accounts slightly improve relationship outcomes, but the research shows that financial communication quality matters far more than account structure. A couple that talks openly about money with separate accounts will do better than a couple with joint accounts who avoid financial conversations.

For couples planning a wedding, the financial setup conversation should happen before the ceremony. See startweddingplanning.com for a complete pre-wedding financial checklist that includes account setup timing.

Decision Framework: Which Approach for You?

Work through these questions to determine your best approach:

Question 1: How similar are your spending styles?

- Very similar → Fully joint works well

- Somewhat different → Hybrid with personal allowances

- Very different → Hybrid with clear personal spending protection

Question 2: What is your income ratio?

- Equal (within 20%) → Any approach works; choose based on preference

- One earns 50-100% more → Hybrid with proportional contribution

- One earns 2× or more → Hybrid with equal personal allowance (not 50/50 joint expenses)

Question 3: How important is financial independence to each partner?

- Both value shared finances → Joint or hybrid

- At least one strongly values independence → Hybrid or separate

Question 4: Are you married or legally partnered?

- Married → Hybrid or joint simplifies tax, legal, and emergency situations

- Unmarried → Separate or hybrid with clear written agreements

Question 5: How is your financial communication right now?

- Open and comfortable → Any approach works; joint adds simplicity

- Improving but still awkward → Hybrid gives structure while building trust

- Tense or avoidant → Start with separate and build toward hybrid as communication improves

If you and your partner are recently married and considering combining finances, our guide on how to combine finances after marriage walks through the transition step by step.

Best Budgeting Tools and Books for Couples

Managing shared finances is easier with the right tools. Here are the budgeting apps, banking tools, and books that work best for couples navigating joint and separate accounts.

YNAB (You Need A Budget)

Best budgeting app for couples — shared budget visibility, real-time syncing, goal tracking across joint and individual accounts. $14.99/month or $99/year.

YNAB Budgeting Guides on AmazonHoneydue

Purpose-built for couples — see shared and individual accounts in one view, set bill reminders together, and chat about transactions in-app. Free.

Financial Planning Guides on AmazonGoodbudget

Envelope budgeting for couples — share digital "envelopes" across devices, perfect for managing the hybrid approach with visible spending categories. Free tier available.

Envelope Budget Systems on AmazonThe One-Page Financial Plan (Book)

By Carl Richards — a quick, practical read for couples who want to get on the same financial page without overwhelming detail. Great for sparking the money conversation.

View on AmazonSmart Couples Finish Rich (Book)

By David Bach — covers joint vs separate accounts, retirement planning as a couple, and the "Latte Factor" for shared expenses. A comprehensive couples finance guide.

View on AmazonCouples Money Management Workbook

Hands-on worksheets for setting up joint budgets, calculating proportional contributions, and planning monthly money dates. Great companion to the hybrid approach.

Money Workbooks on AmazonFor a deeper comparison of budgeting apps built specifically for two-person households, see our full review of the best budgeting apps for couples.

Recommended Banks for Couples

Choosing the right bank matters when you're setting up joint accounts. Here's what to look for and which banks serve couples best in 2026.

Ally Bank

Best overall — high-yield savings (4%+ APY), no monthly fees, easy joint account setup, and a clean mobile app both partners can use. Buckets feature lets you organize savings goals within one account.

Budgeting Books on AmazonChime

Best for automatic savings — SpotMe overdraft protection up to $200, automatic round-up savings, and fee-free overdraft coverage. No monthly fees, no minimum balance.

Finance Workbooks on AmazonChase Total Checking

Best for branch access — 4,700+ branches nationwide, easy joint account opening in person, wide ATM network. $12/month fee waived with direct deposit or minimum balance.

Finance Books on AmazonHow to choose: If you want the highest savings yield and don't need branches, go with Ally. If automatic savings features matter most, Chime is excellent. If either partner prefers in-person banking, Chase or Bank of America give you physical branch access. The best bank is the one both partners will actually use consistently.

Common Mistakes to Avoid

| Mistake | Why It Causes Problems | What to Do Instead |

|---|---|---|

| Never talking about money openly | Financial secrets compound into crises | Monthly 30-min "money date" to review spending |

| 50/50 split on very unequal incomes | Lower earner is financially stressed | Proportional contribution based on income |

| Keeping emergency fund in joint account | Risk of loss if relationship ends | Individual emergency funds + joint savings for goals |

| No "personal spending" allocation | Financial guilt, feeling monitored | Equal personal allowances regardless of income |

| Merging finances before establishing trust | Very difficult to unmerge if problems arise | Hybrid approach first, fully joint after years of trust |

| No written agreement for unmarried couples | Legal complications if relationship ends | Document your financial arrangement |

| Ignoring debt when setting contributions | One partner carries unfair burden | Factor existing debt payments into contribution calculations |

The "Money Date" Habit

The single most effective thing couples can do for their financial health — regardless of account structure — is schedule a recurring monthly money date. This is a 30-minute check-in where you review the previous month's spending, adjust the upcoming month's budget, and discuss any financial concerns or goals. Keep it casual: order takeout, pour a glass of wine, and treat it as a partnership ritual rather than an audit. Couples who do this consistently report dramatically fewer money arguments.

Setting Up Your System

Week 1: Agree on Approach

- Have the "money conversation" — talk through the decision framework above

- Agree on the hybrid, joint, or separate approach

- Set your joint expense budget and personal allowance amounts

- Write down the numbers: total joint expenses, each person's contribution amount, personal allowance per person

Week 2: Open Accounts

- Open a joint checking account for shared expenses

- Consider a joint high-yield savings account for shared goals

- Keep or open individual accounts for personal spending

- Set up automatic transfers: payday → joint account + personal account

Week 3: Set Up Bill Pay

- List all shared bills and their due dates

- Set up automatic payments from the joint account

- Cancel any individual payments being split manually

- Set up a shared spreadsheet or budgeting app to track joint expenses

Week 4: First Monthly Review

- Review spending together during your first money date

- Adjust contribution amounts if joint expenses exceeded the budget

- Note any categories that need discussion

- Celebrate getting the system running — this is a meaningful relationship step

Month 2 and Beyond

- Continue monthly money dates

- Review and adjust quarterly as circumstances change (raises, new expenses, seasonal costs)

- Revisit the overall approach annually — what worked at the start may need tweaking as your relationship and finances evolve

Frequently Asked Questions

Should couples have joint or separate bank accounts?

The hybrid approach works best for most couples: joint for shared expenses, separate for personal spending. Research shows fully joint accounts correlate with slightly higher relationship satisfaction, but financial communication quality matters more than account structure. The right answer depends on your income ratio, spending styles, and how much financial independence each partner needs.

What percentage of couples have joint bank accounts?

43% fully joint, 23% fully separate, 34% hybrid — per 2023 Bankrate survey. The trend is moving toward hybrid arrangements, particularly among younger couples. Among millennials and Gen Z in committed relationships, hybrid accounts are now the most popular choice.

What happens to a joint account if we break up?

Either holder can withdraw all funds at any time. Keep emergency savings individual or with legal protection (prenup, trust). Use joint accounts for expense flow-through, not large balances. If you are concerned about this risk, limit the joint account balance to one to two months of shared expenses and keep larger savings in individual accounts.

How should couples split expenses with different incomes?

Proportional contribution: each contributes based on their income percentage. Plus equal personal spending allowances regardless of income — this prevents the lower earner from feeling financially controlled. For a detailed walkthrough of this calculation, see our guide on how to combine finances after marriage.

Do joint bank accounts affect credit scores?

Bank accounts don't affect credit scores. Joint credit cards and loans do. However, if a joint checking account goes into overdraft and the negative balance is sent to collections, that can appear on both account holders' credit reports. Keep your joint account funded to avoid this risk.

When should we start merging finances?

There is no universal timeline. Many couples start with a trial hybrid account for three to six months before expanding. The key indicators you are ready: you have had multiple open money conversations, you trust each other's financial judgment, and you have a shared financial goal (saving for a home, planning a wedding, building an emergency fund). Rushing into fully joint finances before building financial trust can create more problems than it solves.

Can you have both joint and separate accounts?

Yes — this is exactly the hybrid approach, and it is the most recommended setup. Most banks allow you to hold both joint and individual accounts simultaneously. You can even have joint checking for expenses and joint savings for shared goals alongside your personal accounts.

Sources and Methodology

Research References:

- Gladstone JJ, et al. "Pooling finances and relationship satisfaction." Journal of Personality and Social Psychology, 2018.

- Garbinsky EN, et al. "Shared financial accounts, happiness, and relationship satisfaction." Northwestern University Working Paper, 2023.

- Bankrate: "Money and Relationships Survey," 2023.

- APA: "Stress in America Survey — Financial Stressors and Relationships," 2022.

- National Endowment for Financial Education: "Financial Deception in Relationships," 2023.

By Emma Walsh, Certified Financial Planner

Emma Walsh is a certified financial planner specializing in couple and family financial planning. This site may earn commissions from qualifying purchases. Last updated March 2026.