Guide

Saving for a House as a Couple: Step-by-Step Plan (2026)

A complete step-by-step plan for couples saving for a house in 2026. Learn how to set a down payment goal, build a joint savings strategy, cut expenses together, and stay aligned on your homeownership timeline.

Saving for a house as a couple requires a clear financial plan, honest conversations about money, and consistent action over months or years. This step-by-step guide breaks down exactly how to calculate your target, build a joint savings strategy, choose the right accounts, and stay on track together — whether you are buying your first home or upgrading to accommodate a growing family.

By Olivia Grant, Certified Financial Planner | Last updated March 2026

Table of Contents

- Why Saving for a House Together Is Different

- Step 1: Have the Money Talk Before the Numbers

- Step 2: Calculate Your Total Homebuying Target

- Step 3: Audit Your Current Financial Position

- Step 4: Build Your Joint Savings Strategy

- Step 5: Open the Right Savings Accounts

- Step 6: Cut Expenses and Boost Income Together

- Step 7: Tackle Debt Before or During Your Savings Journey

- Step 8: Protect Your Down Payment Fund

- Step 9: Track Progress and Stay Motivated

- Best Tools and Apps for Couples Saving for a House

- Common Mistakes Couples Make When Saving for a House

- Frequently Asked Questions

- Sources and Methodology

Why Saving for a House Together Is Different

Buying a home is the largest purchase most couples will ever make. According to the National Association of Realtors, the median existing-home sales price in the United States reached $407,500 in early 2026. In Australia, CoreLogic data puts the national median dwelling value at approximately $810,000 AUD.

These are not numbers you casually save for. They demand coordination, discipline, and — critically — partnership.

Saving for a house as a couple is fundamentally different from saving solo. You are merging two income streams, two spending habits, two risk tolerances, and two sets of financial obligations. One partner might carry student loan debt while the other has been saving since their first job. One might be risk-averse and want 20% down; the other might prefer a smaller deposit to get into the market sooner.

The couples who succeed at this are not the ones who earn the most. They are the ones who communicate openly, agree on a plan, and hold each other accountable week after week.

This guide gives you that plan.

Step 1: Have the Money Talk Before the Numbers

Before you open a spreadsheet or a savings account, sit down and have an honest conversation. This is the foundation everything else builds on.

Questions Every Couple Should Answer Together

- When do you want to buy? Agree on a realistic timeline: 1 year, 2 years, 3–5 years.

- Where do you want to live? Location determines price range more than anything else. A house in rural Queensland costs a fraction of one in Sydney's inner west.

- What kind of property? Apartment, townhouse, standalone home — each has different price points and ongoing costs.

- How much are you comfortable borrowing? Some couples want to minimise their mortgage; others are comfortable with higher leverage.

- What are your non-negotiables? Number of bedrooms, proximity to work, school catchment, garden space.

- What is each person's current financial situation? Debts, savings, credit score, income stability.

Why This Conversation Matters

A 2025 Fidelity Investments survey found that 43% of couples disagree on how much they have saved, and 36% cannot agree on when they will be ready to retire. If couples are misaligned on basic savings numbers, imagine the disconnect when a six-figure home purchase is involved.

Get on the same page now. Write down your agreed answers. Revisit them every quarter.

Step 2: Calculate Your Total Homebuying Target

Most people think "down payment" when they think about saving for a house. But the down payment is only one piece. You need to budget for the full cost of buying and moving into a home.

The Complete Cost Breakdown

| Cost Category | Typical Range | Example ($400,000 Home) |

|---|---|---|

| Down payment (20%) | 5–20% of price | $80,000 |

| Closing costs | 2–5% of price | $8,000–$20,000 |

| Home inspection | $300–$600 | $450 |

| Appraisal fee | $300–$500 | $400 |

| Moving costs | $1,000–$5,000 | $2,500 |

| Immediate repairs | 1–2% of price | $4,000–$8,000 |

| Emergency reserve | 3–6 months expenses | $10,000–$18,000 |

Total liquid cash needed for a $400,000 home: approximately $105,000–$129,000.

That number is larger than most couples expect. But knowing it upfront prevents the painful surprise of realising you are $20,000 short three weeks before settlement.

Down Payment: How Much Do You Actually Need?

The 20% down payment is the gold standard because it eliminates private mortgage insurance (PMI) in the US and lenders mortgage insurance (LMI) in Australia. But it is not the only option.

US options:

- FHA loan: 3.5% down (minimum credit score 580)

- Conventional loan: 3–5% down (with PMI, typically $100–$300/month)

- VA loan: 0% down (for veterans and active military)

- USDA loan: 0% down (for rural areas)

Australian options:

- Standard deposit: 20% to avoid LMI

- First Home Guarantee: 5% deposit (government guarantees the rest — limited places)

- First Home Super Saver Scheme: Withdraw voluntary super contributions for a deposit

Putting down less than 20% gets you into a home sooner but costs more over the life of the loan. A couple putting 5% down on a $400,000 home pays roughly $150–$250 per month in PMI until they reach 20% equity. Over five years, that is $9,000–$15,000 in extra costs.

Run the numbers both ways. For many couples in high-cost markets, getting in sooner with a smaller deposit and building equity through appreciation may actually be the better financial move — especially if rents are high and rising.

Step 3: Audit Your Current Financial Position

You cannot build a savings plan without knowing where you stand today. This step requires transparency — both partners need to lay their finances on the table.

What to Calculate Together

Combined monthly income (after tax): Add both take-home pay amounts. Include any reliable side income, but do not count sporadic or uncertain sources.

Combined monthly expenses: Track every dollar for at least one month. Use your bank statements or a budgeting app like Monarch Money or YNAB. Categorise spending into needs (rent, utilities, groceries, insurance, minimum debt payments), wants (dining out, subscriptions, entertainment), and savings.

Existing savings: What do you have right now that could go toward the house fund? Include savings accounts, term deposits, investment accounts you would liquidate, and any gifts from family.

Outstanding debts: List every debt: student loans, car loans, credit cards, personal loans, buy-now-pay-later balances. Note the balance, interest rate, and minimum payment for each.

Credit scores: Both partners should check their credit scores. In the US, aim for 700+ for the best mortgage rates. In Australia, check your credit report through Equifax or Illion.

The Gap Analysis

Once you have these numbers, the math is simple:

Monthly savings capacity = Combined income − Combined expenses

Time to goal = (Total target − Current savings) ÷ Monthly savings capacity

If your target is $100,000, you have $15,000 saved, and you can save $2,500 per month, your timeline is 34 months — just under three years.

If that timeline does not match when you want to buy, you have three levers to pull: increase income, decrease expenses, or adjust your target (smaller deposit, less expensive home, different location).

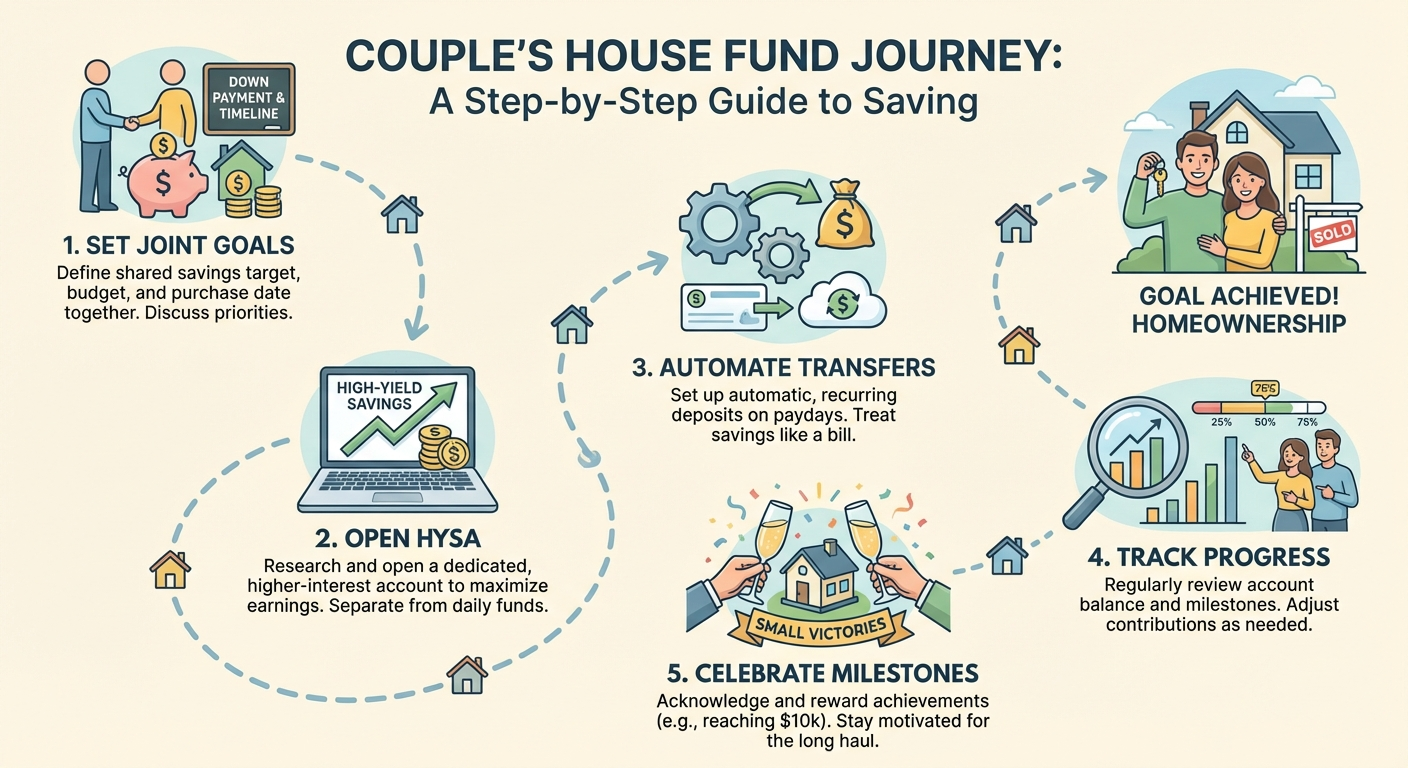

Step 4: Build Your Joint Savings Strategy

This is where the plan gets real. You need to decide how much each person contributes, how often, and where the money goes.

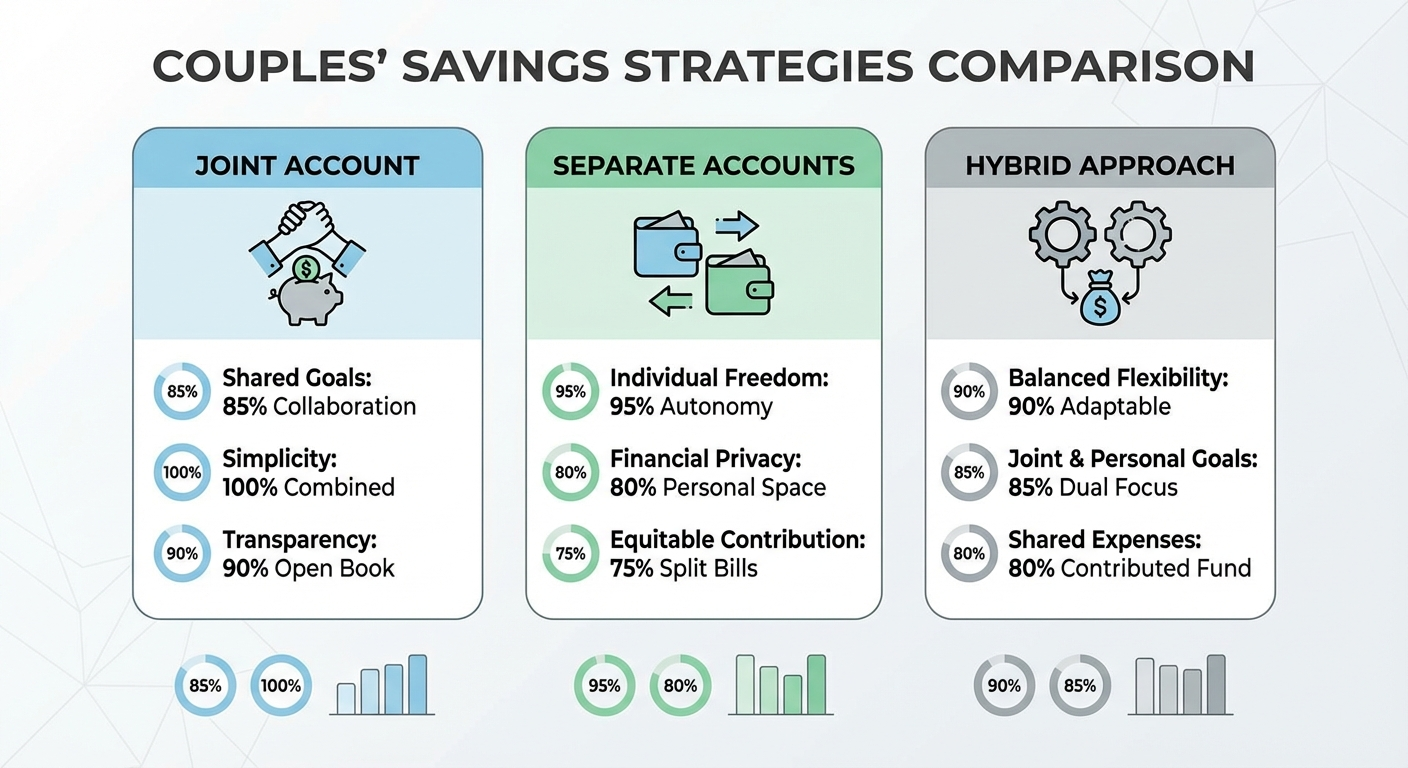

Choosing a Contribution Model

Option 1: Equal contributions (50/50) Each partner puts the same dollar amount toward the house fund every month. Simple and clear, but can feel unfair if there is a significant income gap.

Option 2: Proportional contributions (recommended) Each partner contributes a percentage of their income. If Partner A earns $75,000 and Partner B earns $45,000, Partner A contributes 62.5% of the savings target and Partner B contributes 37.5%. This is the most equitable approach for couples with different incomes.

Option 3: One saver, one bill payer One partner covers all household bills while the other funnels their entire income into savings. This can accelerate the timeline dramatically but requires trust and clear agreements.

Setting Your Monthly Savings Target

Work backwards from your goal:

- Target amount: $100,000

- Current savings: $15,000

- Remaining: $85,000

- Desired timeline: 30 months

- Monthly target: $2,833

Now divide that monthly target according to your chosen contribution model. Set up automatic transfers on payday — not at the end of the month when the money might already be spent.

The Pay-Yourself-First Rule

The most effective savings strategy is also the simplest: automate your savings before you have a chance to spend the money. Set up automatic transfers to your house fund on the same day your pay hits your account. Treat this transfer like a bill — non-negotiable.

Couples who automate their savings are 2–3 times more likely to reach their goals than those who save "whatever is left over" at the end of the month, according to research from the Consumer Financial Protection Bureau.

Step 5: Open the Right Savings Accounts

Where you park your down payment matters. The wrong account can cost you thousands in missed interest or expose your savings to unnecessary risk.

High-Yield Savings Accounts (HYSA)

For most couples saving for a house within 1–5 years, a high-yield savings account is the best choice. As of March 2026, the best HYSAs in the US offer 4.0–4.5% APY, and Australian savings accounts offer 5.0–5.5% with bonus interest.

What to look for:

- APY of 4%+ (US) or 5%+ (Australia)

- No monthly fees

- No minimum balance requirement

- Joint account option (both partners have access)

- FDIC insured (US) or ADI protected (Australia)

- Easy transfer in and out

On a $50,000 balance earning 4.5% APY, you earn roughly $2,250 per year in interest — money that compounds and accelerates your timeline.

Where NOT to Put Your Down Payment

Individual stocks or crypto: Too volatile. A 20% market drop could delay your purchase by years.

Long-term CDs/term deposits: Your money is locked up. If you find the right house before the CD matures, you pay early withdrawal penalties.

Your everyday checking account: Too easy to spend. Down payment funds should be separate and visible but not immediately accessible for impulse purchases.

Under the mattress: You are losing purchasing power to inflation every month.

Consider a Dedicated House Fund

Open a savings account that is exclusively for your home purchase. Name it "House Fund" or "Our First Home" — many banks let you name sub-accounts. The psychological impact of watching a dedicated account grow is powerful motivation.

If you already use a budgeting app like Monarch Money, you can create a savings goal within the app and track your progress visually. Seeing that progress bar inch toward 100% keeps both partners engaged.

Step 6: Cut Expenses and Boost Income Together

Once you have your savings target, look for ways to close the gap faster. This is where teamwork makes the biggest difference.

Expenses to Cut First (Highest Impact)

Housing costs (your current rent): Can you downsize temporarily? Move to a less expensive area? Get a roommate? Even saving $400/month on rent for two years adds $9,600 to your house fund.

Transportation: Can you go from two cars to one? Switch to public transport? Refinance a car loan at a lower rate? The average American spends $12,182 per year on transportation, according to the Bureau of Labor Statistics.

Subscriptions and recurring charges: Audit every subscription. Cancel anything you have not used in the past month. The average American household spends $219/month on subscriptions — that is $2,628/year.

Dining out and food delivery: This is typically the largest discretionary spending category for couples. Cooking at home more often can save $200–$500/month easily. If you are looking for ways to reduce your grocery bill, meal planning as a couple can cut food waste and spending significantly.

Entertainment and travel: You do not have to eliminate fun. But shifting from expensive holidays to local adventures, from concert tickets to free community events, can free up thousands per year.

Ways to Boost Income

Negotiate a raise: The best time to ask is after a strong performance review. Even a 5% raise on a $70,000 salary adds $3,500/year.

Side income: Freelancing, tutoring, driving for rideshare, selling items you no longer need. Even $500/month extra cuts your timeline by months.

Windfalls: Tax refunds, bonuses, gift money, inheritance — funnel 100% of unexpected money into the house fund. A couple who directs two annual tax refunds of $3,000 each into savings adds $12,000 over two years.

Employer matching: If your employer offers retirement matching, make sure you are getting the full match. That is free money. But do not over-contribute to retirement at the expense of your house fund — you can always increase retirement contributions after you buy.

Step 7: Tackle Debt Before or During Your Savings Journey

Debt does not automatically disqualify you from buying a home, but it affects how much you can borrow and at what interest rate. Lenders look at your debt-to-income ratio (DTI) — the percentage of your gross monthly income that goes toward debt payments.

Understanding Debt-to-Income Ratio

Most lenders want your total DTI (including the proposed mortgage payment) to be below 43%. Some prefer 36% or lower.

Example:

- Combined gross monthly income: $10,000

- Current debt payments: $800/month (student loans + car payment)

- Proposed mortgage payment: $2,200/month

- DTI: ($800 + $2,200) ÷ $10,000 = 30% ✅

If your DTI is too high, you either need to pay down debt or reduce the size of the mortgage you are applying for.

The Debt vs. Savings Decision

Should you pay off all debt before saving for a house? It depends on the interest rate.

Pay off first (interest rate above 7%): Credit card debt, personal loans, buy-now-pay-later — these carry high interest that erodes your financial position faster than savings can grow. Prioritise eliminating these.

Pay minimums and save simultaneously (interest rate below 7%): Student loans, car loans with reasonable rates — continue making minimum payments while directing extra cash to your house fund. The interest you are paying is likely lower than the long-term benefit of getting into the housing market.

Never stop paying minimums on anything. Missed payments damage your credit score, which directly affects the mortgage rate you will be offered.

Step 8: Protect Your Down Payment Fund

You have been saving diligently for months. The last thing you want is an unexpected expense wiping out your progress.

Keep a Separate Emergency Fund

Do not use your house fund as your emergency fund. They serve different purposes.

Your emergency fund (3–6 months of expenses) covers job loss, medical bills, car repairs, and other surprises. Your house fund is exclusively for the purchase.

If you drain your house fund to cover an emergency, you reset your timeline and lose the compound interest you had built up. Keep them in separate accounts.

Insurance Review

Make sure you have adequate health insurance, car insurance, and renter's insurance. An uninsured medical bill or car accident can destroy months or years of savings progress.

Avoid Lifestyle Inflation

As your income grows, resist the urge to upgrade your lifestyle. Every raise, bonus, or side income increase should flow into savings — not into a bigger apartment, a newer car, or more expensive restaurants.

The period while you are saving for a house is temporary. Living below your means now funds the life you want later.

Step 9: Track Progress and Stay Motivated

Saving for a house is a marathon, not a sprint. Most couples take 2–5 years to accumulate a sufficient down payment. Staying motivated over that period requires intentional effort.

Monthly Check-Ins

Schedule a monthly "money date" with your partner. Review your progress, celebrate milestones, and adjust the plan if needed. Keep these meetings positive — focus on how far you have come, not just how far you have to go.

What to review each month:

- Total in house fund vs. target

- Did you hit your monthly savings goal?

- Any unexpected expenses that affected savings?

- Changes to income or expenses coming up?

- Is the timeline still realistic?

Visual Progress Tracking

Create a visual tracker that you both see daily. This could be a thermometer chart on the fridge, a progress bar in your budgeting app, or a simple spreadsheet chart.

Research from the Dominican University of California found that people who write down their goals and track progress are 42% more likely to achieve them. Making your progress visible keeps the goal front of mind.

Celebrate Milestones

Set intermediate milestones and celebrate when you hit them:

- $10,000 saved: Cook a special dinner at home

- $25,000 saved: Have a low-cost date night out

- $50,000 saved: Plan a day trip adventure

- Halfway point: Write each other a letter about what the house means to you

- Goal reached: Open the champagne

These celebrations do not have to cost much. The point is to acknowledge the sacrifice and discipline that got you there.

Best Tools and Apps for Couples Saving for a House

The right tools make the process easier and more transparent. Here are the best options for couples working toward homeownership.

Clever Fox Budget Planner for Couples

Best for: Couples who prefer pen-and-paper budgeting

Price: $23–$30

Check on Amazon →Cash Envelope Budget System

Best for: Controlling discretionary spending while saving

Price: $15–$25

Check on Amazon →

Savings Goal Tracker Whiteboard

Best for: Visual progress tracking at home

Price: $18–$35

Check on Amazon →The House Hacking Strategy by Craig Curelop

Best for: Couples considering house hacking to build equity faster

Price: $15–$22

Check on Amazon →Nolo's Essential Guide to Buying Your First Home

Best for: Understanding the full homebuying process

Price: $20–$28

Check on Amazon →Digital Tools

Monarch Money — Best overall budgeting app for couples. Supports shared dashboards, joint goals, and individual privacy. Create a dedicated "House Fund" goal and track progress together. Costs $14.99/month or $99.99/year.

YNAB (You Need a Budget) — Best for zero-based budgeting. Every dollar gets a job, which is perfect for aggressive saving. Excellent couples features. Costs $14.99/month or $109/year.

Honeydue — Best free option. Purpose-built for couples. Tracks shared bills, lets you set spending limits, and shows both accounts in one view. Free with optional premium features.

If you want a detailed comparison of all the top apps, check out our guide to the best budgeting apps for couples.

Common Mistakes Couples Make When Saving for a House

Mistake 1: Not Having a Written Plan

"We will just save as much as we can" is not a plan. Without a specific target, timeline, and monthly contribution amount, savings drift. One partner might think you are on track while the other is stressed about being behind. Write it down. Share it. Refer to it monthly.

Mistake 2: Ignoring the Full Cost of Homeownership

The mortgage payment is not your only cost. Property taxes, insurance, maintenance (budget 1–2% of home value per year), HOA fees, and utilities can add $500–$1,500 per month on top of your mortgage. Make sure your budget accounts for these ongoing costs before you commit to a purchase price.

Mistake 3: Draining Your Emergency Fund for the Down Payment

If you empty your emergency fund to buy a house, the first major repair or unexpected expense puts you into debt — potentially high-interest credit card debt. Always maintain at least 3 months of expenses as a buffer.

Mistake 4: Not Checking Both Credit Scores Early

Your mortgage rate depends on both credit scores if you are applying jointly. A score of 620 versus 760 can mean the difference of 1–2 percentage points on your interest rate — costing tens of thousands over the life of the loan. Check both scores early and take action to improve them before you apply.

Mistake 5: Saving in the Wrong Account

Keeping your house fund in a regular checking account earning 0.01% means you are losing money to inflation every month. A high-yield savings account earning 4.5% on $80,000 generates $3,600 per year in interest. That is essentially free money toward your goal.

Mistake 6: Making Major Financial Changes Before Closing

Do not open new credit cards, finance a car, change jobs, or make large purchases in the months before applying for a mortgage. Lenders re-check your financial profile before closing, and any changes can delay or derail your approval.

Getting Pre-Approved: When Your Savings Are Ready

Once you have accumulated 80–90% of your target savings, it is time to start the pre-approval process. Pre-approval is not the same as pre-qualification — it involves a full credit check and income verification, and it gives you a concrete number for what a lender will offer.

What You Need for Pre-Approval

- Proof of income: Pay stubs (last 30 days), W-2s or tax returns (last 2 years)

- Bank statements: Last 2–3 months showing your savings

- Employment verification: Letter from employer or contract

- Credit report: Lender pulls this directly

- Debt documentation: Statements for all outstanding debts

- Identification: Government-issued ID for both partners

Shop Multiple Lenders

Do not accept the first offer. Get pre-approval quotes from at least 3 lenders — your bank, a credit union, and an online lender. Even a 0.25% difference in interest rate saves thousands over a 30-year mortgage.

If you are concerned about multiple credit inquiries, know that mortgage-related credit checks within a 14–45 day window (depending on the scoring model) count as a single inquiry. Shop aggressively within that window.

How to Handle Different Financial Situations

When One Partner Has Significantly More Savings

This is common and not a problem — as long as you discuss it openly. Options include:

- Pool everything: Both partners contribute all savings to the joint fund. Simple but requires high trust.

- Match contributions going forward: The partner with more savings contributes what they have; going forward, both contribute equally or proportionally.

- Legal protection: Consider a cohabitation agreement or prenup that documents each partner's contribution. This protects both parties if the relationship changes.

When One Partner Has Bad Credit

If one partner's credit score is significantly lower, you have options:

- Apply with only the higher-scoring partner: This can get a better rate but limits borrowing power to one income.

- Spend 6–12 months improving the lower score: Pay down credit card balances, dispute errors on credit reports, avoid new credit applications.

- Use the better score for the mortgage and add the other partner to the title: This gives both partners ownership while securing the better rate.

When Incomes Are Very Different

The proportional contribution model (described in Step 4) is fairest here. If you are starting an Etsy shop or side business for extra income, that income can accelerate your timeline — just make sure both partners agree on how side income gets allocated.

Timeline Templates for Different Savings Goals

Aggressive: Buy in 18 Months

- Combined income: $120,000/year after tax

- Target: $80,000

- Monthly savings: $4,444

- Strategy: Extreme expense cutting, side income, downsize current housing, redirect all windfalls

Moderate: Buy in 3 Years

- Combined income: $100,000/year after tax

- Target: $80,000

- Monthly savings: $2,222

- Strategy: Automate savings, reduce dining out and subscriptions, negotiate raises, invest in HYSA

Conservative: Buy in 5 Years

- Combined income: $80,000/year after tax

- Target: $80,000

- Monthly savings: $1,333

- Strategy: Steady automation, gradual expense reduction, focus on career growth for income increases, maximise HYSA interest

The right timeline depends on your market, your income, and your tolerance for short-term sacrifice. There is no shame in a longer timeline if it means buying comfortably without financial stress.

Frequently Asked Questions

How much should a couple save before buying a house?

Most couples should aim to save 20% of the home price for the down payment, plus 3–5% for closing costs, plus a 3–6 month emergency fund. For a $400,000 home, that means roughly $80,000 for the down payment, $12,000–$20,000 for closing costs, and $10,000–$15,000 in reserves — totalling around $102,000–$115,000.

Should couples open a joint savings account for a house down payment?

Yes. A dedicated joint high-yield savings account keeps your down payment fund separate from everyday spending, creates shared visibility, and earns interest. Look for accounts offering 4%+ APY with no monthly fees. Both partners should have equal access and transaction alerts turned on.

How long does it take for a couple to save for a house?

Timeline depends on income, expenses, and target. A couple earning $120,000 combined and saving $2,000 per month could reach a $60,000 down payment in about 2.5 years. Couples who automate savings and reduce discretionary spending often shave 6–12 months off their timeline.

What is the best budgeting method for saving for a house?

The 50/30/20 rule adapted for homeownership works well: 50% on needs, 20% on wants (reduced from 30%), and 30% toward savings including your down payment fund. Zero-based budgeting with apps like YNAB or Monarch Money gives couples even more control over every dollar. For a deeper dive into this approach, see our guide to the 50/30/20 budget rule for couples.

Can you buy a house with less than 20% down?

Yes. FHA loans require as little as 3.5% down, and conventional loans may accept 5–10%. However, putting down less than 20% typically means paying private mortgage insurance (PMI), which adds $100–$300 per month to your costs. Saving more upfront reduces long-term costs significantly.

How do couples handle different incomes when saving for a house?

The proportional contribution method is fairest. Each partner contributes a percentage of their income rather than a fixed dollar amount. If one partner earns 60% of the household income, they contribute 60% of the monthly savings target. This keeps the burden equitable without resentment. Read more about contribution models in our guide to combining finances after marriage.

Sources and Methodology

This article draws on data and research from the following sources:

- National Association of Realtors (NAR) — Median home price data, buyer demographics, and market trends (2025–2026 reports).

- CoreLogic Australia — National dwelling value index and housing market data (Q1 2026).

- Consumer Financial Protection Bureau (CFPB) — Research on automated savings and financial behaviour.

- Fidelity Investments Couples & Money Study (2025) — Survey data on financial alignment in relationships.

- American Psychological Association (APA) — Stress in America survey data on financial stress.

- Bureau of Labor Statistics (BLS) — Consumer Expenditure Survey data on transportation and housing costs.

- Ramsey Solutions — Research on money conflicts and divorce rates.

- Dominican University of California — Study on goal setting and written accountability.

- Federal Housing Administration (FHA) — Current loan requirements and down payment minimums.

- Australian Government — Treasury — First Home Guarantee and First Home Super Saver Scheme guidelines.

All statistics cited are from 2024–2026 publications. Interest rates and account yields quoted are accurate as of March 2026 and may vary by institution.

Olivia Grant is a Certified Financial Planner specialising in couples finance and homeownership planning. She has helped over 200 couples navigate the path to their first home purchase. Olivia writes for Budgeting for Couples to make financial planning accessible and actionable for real partnerships.