Budgeting

Budgeting with One Income: Practical Strategies (2026)

Learn how to budget with one income. Practical strategies for single-income families to manage money, cut costs, and build financial security in 2026.

Living well on a single income is not just possible—it can be deeply rewarding when you have the right strategy. Managing a household budget with one income requires more intention, more planning, and more communication than a two-income home, but couples who master it often report stronger financial foundations and less money-related stress. This comprehensive guide walks you through every aspect of single-income budgeting, from setting up your first budget to protecting your family's future with insurance and retirement planning.

Last updated: April 2026

Table of Contents

- Why Budgeting with One Income Is More Common Than You Think

- The 50/30/20 Rule Adapted for Single-Income Households

- Building Your One-Income Budget from Scratch

- Cutting Costs Without Sacrificing Quality of Life

- Emergency Funds and Debt Management on One Income

- Protecting Your Family: Insurance and Safety Nets

- Planning for the Future: Retirement and Kids' Education

- How to Stay Motivated and Avoid Budget Burnout

- Frequently Asked Questions

- Sources & Methodology

Why Budgeting with One Income Is More Common Than You Think

According to the U.S. Census Bureau, approximately 30% of American households with children rely on a single income earner. Similar trends appear across Australia, the United Kingdom, and Canada. Some couples choose single-income households because childcare costs make dual incomes economically inefficient. Others find that one partner's career demands—such as frequent relocation, intense travel schedules, or extended hours—make it impractical to maintain two roles in the workforce.

Whatever your reason for living on one income, the financial principles remain consistent: you need more precision, more deliberate allocation, and more ongoing communication than households with multiple paychecks. The good news is that the strategies used by the most successful single-income families are accessible to anyone willing to invest the time.

Research from the Financial Resilience Institute found that single-income families who maintain a written budget are 2.3 times more likely to report feeling financially secure compared to those who do not. A budget is not a restriction—it is a tool that gives you permission to spend confidently in the areas that matter most to your family while protecting your financial future.

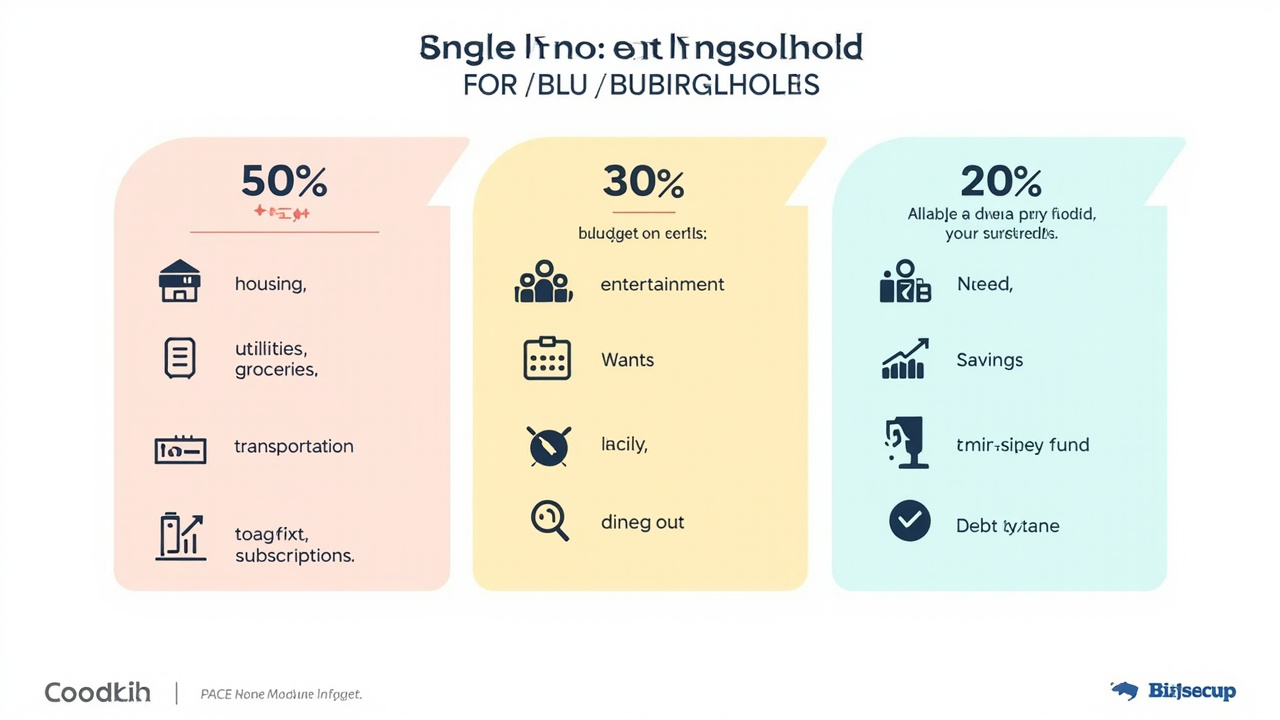

The 50/30/20 Rule Adapted for Single-Income Households

The 50/30/20 rule, popularized by Senator Elizabeth Warren, provides a simple framework for dividing after-tax income into three broad categories:

- 50% for Needs — housing, utilities, groceries, insurance, minimum debt payments, childcare

- 30% for Wants — entertainment, dining out, hobbies, subscriptions, personal spending

- 20% for Savings and Extra Debt Payoff — emergency fund, retirement contributions, extra debt payments

For single-income households, the traditional 50/30/20 split often needs adjustment. When one income must cover everything, many families find that a 60/20/20 split—or even 60/15/25—provides better balance, dedicating slightly more to essential needs while protecting savings.

Adjusted 50/30/20 for Single-Income Families

| Category | Traditional | Single-Income Adjusted |

|---|---|---|

| Needs | 50% | 55–60% |

| Wants | 30% | 15–20% |

| Savings & Debt | 20% | 20–25% |

The key is to calculate your actual numbers before committing to any ratio. Take your monthly after-tax income and list every fixed expense—rent or mortgage, car payment, insurance premiums, utilities, loan minimums. The remainder is what you can allocate to flexible categories and savings.

For example, if your monthly after-tax income is $5,000:

- Needs cap at $3,000 (60%)

- Wants budget of $750–$1,000 (15–20%)

- Savings and extra debt payments of $1,000–$1,250 (20–25%)

This framing makes it immediately clear where every dollar should go before the month begins. Visit our 50/30/20 budget guide for couples for a deeper exploration of this methodology.

Building Your One-Income Budget from Scratch

Step 1: Calculate Your Total Monthly Income

Start with your net (after-tax) monthly income. If you are salaried, this is straightforward. If you are self-employed or have variable income, use your lowest realistic monthly figure as your baseline and treat extra earnings as bonus allocations to savings or debt payoff.

Step 2: List All Fixed Expenses

Fixed expenses are the non-negotiable costs that appear every month: rent or mortgage, car payments, insurance premiums, phone and internet plans, childcare, union dues, and subscription services. Add them up and subtract from your income. This number is your starting point.

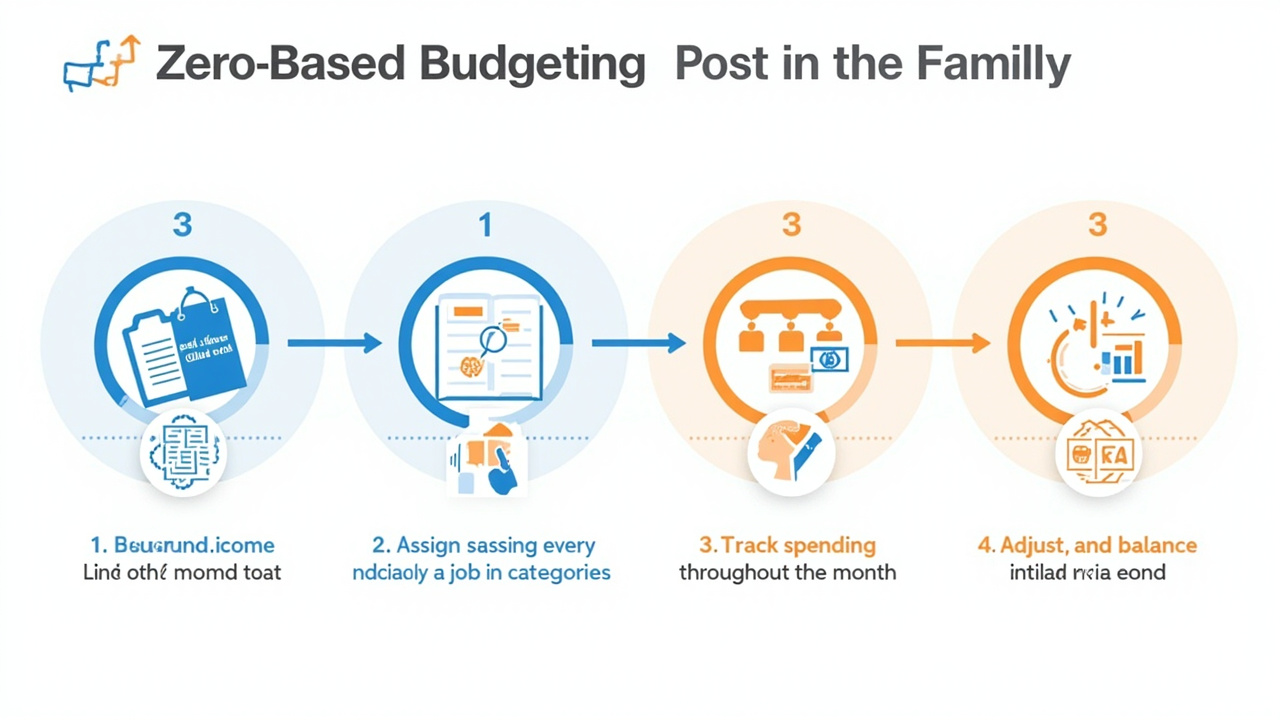

Step 3: Apply the Zero-Based Budget Method

Every dollar gets assigned a job before the month begins. When income minus expenses minus savings minus allocations equals zero, you have given every dollar a purpose. This prevents the passive drift that leads many families to wonder where their money went by the 15th of each month.

Step 4: Track Every Expense for 60 Days

Use a simple spreadsheet or an app like Mint, YNAB, or PocketGuard to record every transaction. After 60 days, review your spending patterns and adjust categories accordingly. Many families are surprised to discover how much they spend on dining out, streaming services, or impulse purchases.

Step 5: Hold a Monthly Budget Meeting

Schedule one hour each month—preferably at the end of the previous month or the first of the new month—to review last month's results and allocate the upcoming month's income. Both partners should attend. Use this meeting to celebrate wins (you stayed under budget in groceries!), identify problem areas (that unexpected car repair), and adjust categories for the coming weeks.

Our guide on how to have a productive money conversation without fighting offers practical communication techniques that make these meetings more productive and less stressful.

Cutting Costs Without Sacrificing Quality of Life

One-income budgeting requires ongoing discipline in reducing unnecessary expenditure. The most effective strategies are those that save significant money without meaningfully reducing your quality of life. Here are the highest-impact changes single-income families can make:

1. Audit and Eliminate Subscription Services

The average Australian household spends $140 per month on streaming and subscription services. Review every subscription—video platforms, music services, gym memberships, subscription boxes—and cancel those you have not used in the past 60 days. Reinstate only the ones that genuinely deliver value.

2. Refinance High-Interest Debt

If you carry credit card debt, explore balance transfer options that offer 0% APR for 12–18 months. Even a $5,000 balance transferred to a 0% card with a 3% transfer fee saves hundreds in interest compared to making minimum payments on a standard 19% card.

3. Negotiate Recurring Bills

Call your insurance provider, internet service company, and mobile carrier and ask for a better rate. Loyalty discounts and promotional offers are regularly available—you just have to ask. This single action can save $50–$200 per month for most households.

4. Cook More Meals at Home

The average Australian family spends $3,500 per year on takeaway and dining out. Reducing this by just $80 per week by cooking more dinner meals at home saves over $4,000 annually. Meal planning is the single biggest driver of home cooking success. For budget-friendly recipes the whole family will enjoy, visit Plan Family Meals for ideas that keep costs down without sacrificing nutrition or taste.

5. Switch to Generic Brands

Supermarket own-brand products are typically manufactured in the same facilities as their name-brand equivalents. Switching to generic groceries in categories like cleaning products, pantry staples, and pantry basics can save 25–40% without any change in quality.

6. Reduce Energy Consumption

Simple changes—switching to LED bulbs, adjusting thermostat settings by 1–2 degrees, unplugging idle electronics, using cold-water laundry cycles—can reduce energy bills by $30–$60 per month without changing your lifestyle.

7. Review Insurance Coverage Annually

Insurance companies regularly offer better rates to new customers than to loyal policyholders. Shop around every 12–18 months for car insurance, home insurance, and health insurance. A 15-minute comparison could save $800–$1,500 per year.

Emergency Funds and Debt Management on One Income

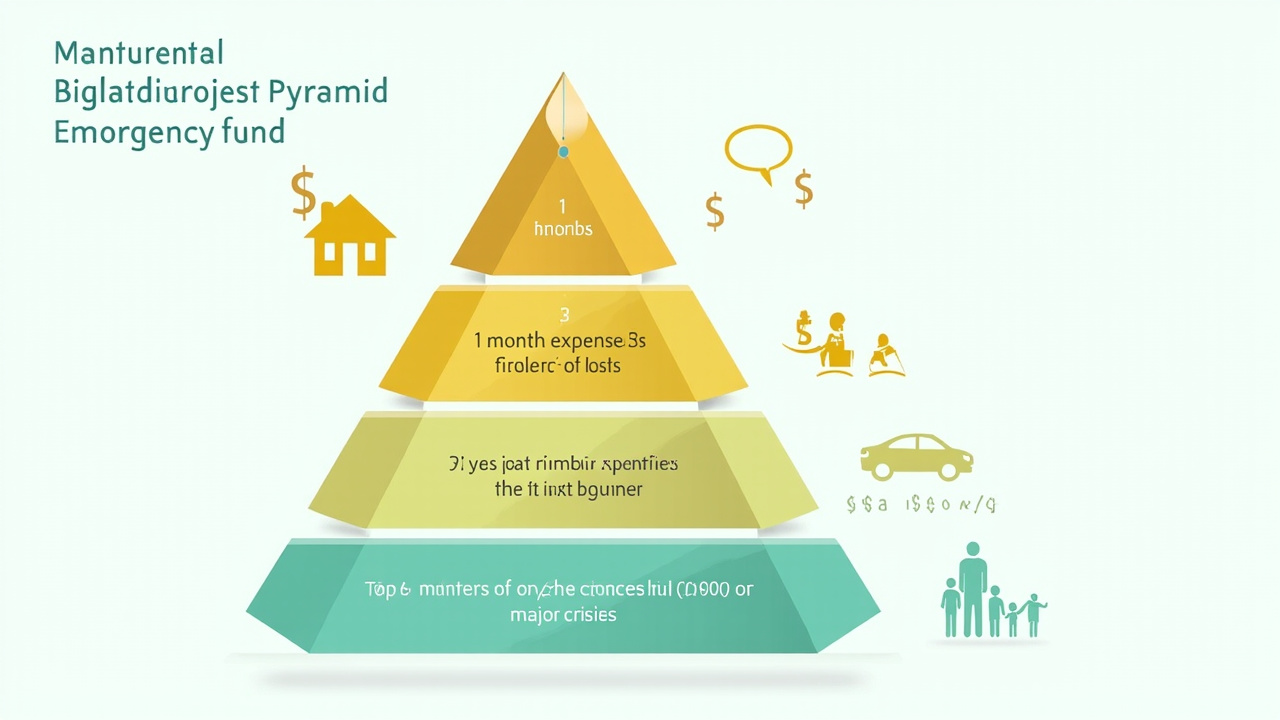

One of the biggest risks single-income families face is the loss of the sole income due to illness, injury, job loss, or death. Building a robust emergency fund is not optional—it is the foundation of financial security.

Tier 1: Starter Emergency Fund ($1,000–$2,000)

Before tackling any debt, build a starter emergency fund of $1,000–$2,000 to cover small unexpected expenses. This prevents minor surprises from adding to credit card debt. Save this within 60–90 days by temporarily reducing discretionary spending.

Tier 2: Full Emergency Fund (3–6 Months of Expenses)

Once your starter fund is in place, grow it to cover 3–6 months of essential household expenses. For a single-income family, aim for 6 months of expenses since the income cannot be quickly replaced. Calculate your essential monthly expenses (housing, utilities, food, insurance, minimum debt payments, childcare) and multiply by six.

The journey from $2,000 to a full 6-month fund can feel long. Use the snowball method: direct any windfalls (tax refunds, bonuses, gifts) straight to the emergency fund, and allocate whatever you save from cost-cutting measures to this goal.

Tier 3: Income Loss Buffer (12 Months of Core Expenses)

For extra security—especially if your profession is more vulnerable to economic downturns—work toward a 12-month buffer in a high-yield savings account. This level of security means a job loss would not be a crisis; it would simply be a matter of activating your budget while you seek new employment.

Managing Debt on One Income

Prioritize debt payoff using the avalanche method: make minimum payments on all debts while directing any extra funds toward the highest-interest debt. This mathematically minimizes total interest paid.

However, if you find yourself losing motivation with the avalanche method, the snowball method—paying off the smallest balance first for a psychological win—can be more effective psychologically. Both methods work; choose the one that keeps you consistent.

Avoid taking on new consumer debt. A single-income household is more vulnerable to compounding interest spirals, particularly if an unexpected expense is placed on a high-interest credit card.

Protecting Your Family: Insurance and Safety Nets

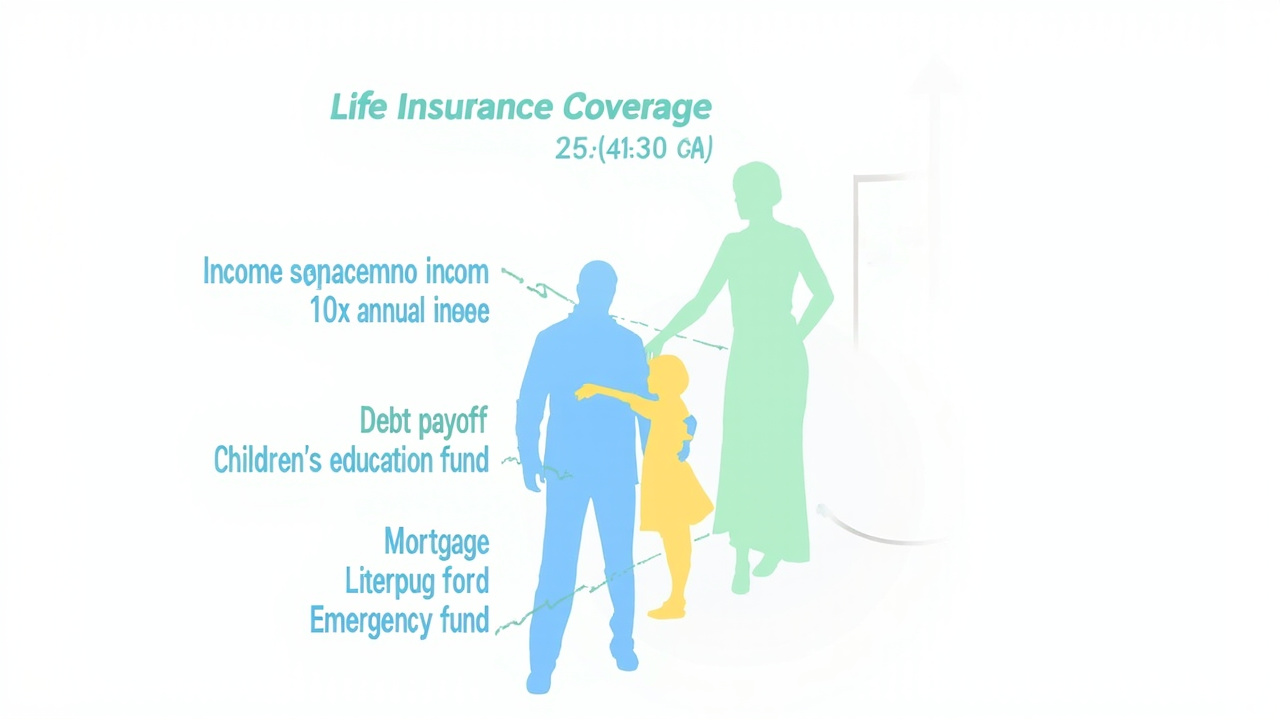

Single-income families face a unique financial risk: the death or disability of the sole earner can eliminate the family's entire income. Insurance is not an optional extra—it is a critical component of responsible single-income financial planning.

Life Insurance

Term life insurance is the most cost-effective protection for single-income families. A policy worth 10–12 times your annual income provides enough to:

- Pay off all outstanding debts (mortgage, car loans, credit cards)

- Cover 3–5 years of living expenses for the surviving spouse and children

- Fund children's education

- Provide for any remaining financial goals

For a family earning $75,000 per year, a 10-year level-term policy with $750,000 of coverage may cost as little as $40–$60 per month at age 30. Costs increase with age and health conditions, which is why purchasing coverage earlier is almost always cheaper.

Income Protection Insurance

If the primary earner becomes unable to work due to illness or injury, income protection insurance replaces a portion of lost earnings. Most policies cover 60–75% of your pre-tax income. Waiting periods and benefit periods vary—shorter waiting periods cost more but begin paying sooner.

Critical Illness Cover

Critical illness insurance provides a lump sum payment if you are diagnosed with a specified serious illness such as cancer, heart attack, or stroke. This money can be used for treatment costs, home modifications, or supplementing lost income during recovery.

Health Insurance

Never skip health insurance. A serious illness or accident without coverage can wipe out years of savings within months. For Australian families, review both public system options and private health insurance to find the right balance of coverage and cost.

Write a Written Partnership Agreement

Many financial planners recommend that single-income couples create a written partnership agreement that clarifies:

- How household expenses are allocated and tracked

- What constitutes a discretionary versus essential purchase

- How financial decisions are made and who has authority

- What happens to finances in various life scenarios (job loss, illness, death)

- Goals for savings, retirement, and children's education

This document is not romantic, but it is practical. It eliminates ambiguity and reduces conflict during stressful financial moments.

Planning for the Future: Retirement and Kids' Education

Retirement Savings: Start Now, Adjust as Needed

The power of compound interest means that time is your most valuable asset in retirement planning. A single-income family saving $500 per month from the birth of their first child until retirement will accumulate significantly more than a family that starts saving the same amount ten years later.

Contribution targets for single-income households:

| Age Range | Target Monthly Contribution (as % of gross income) |

|---|---|

| 25–35 | 15% |

| 35–45 | 18–20% |

| 45–55 | 20–22% |

| 55–65 | 22–25%+ |

Use tax-advantaged accounts: 401(k) employer matches (always contribute at least enough to capture the full match), Roth IRA for tax-free growth, and HSA for medical expenses. In Australia, maximise your superannuation contributions, particularly the government co-contribution if you are eligible.

Children's Education Planning

Saving for children's education while also building retirement savings requires careful prioritisation. Financial advisors consistently recommend funding your own retirement before allocating large sums to education savings. You can borrow for education; you cannot borrow for retirement.

A balanced approach: contribute enough to education savings accounts to capture any government match or tax benefit, while directing the majority of surplus savings to retirement. As retirement goals are met, redirect additional funds to education.

529 plans (US), RESP accounts (Canada), or Australian education savings bonds provide tax-advantaged vehicles for education savings. Starting when your child is born—even with $50–$100 per month—creates meaningful savings over 18 years through compound growth.

How to Stay Motivated and Avoid Budget Burnout

Budgeting on one income is not just about spreadsheets and numbers—it requires a resilient mindset and a clear sense of purpose. Here are strategies to stay motivated for the long term:

Focus on the "Why"

Remind yourself regularly why you chose this path. Whether it is to have one parent present at every childhood milestone, to escape the childcare treadmill, to build a business, or to support a partner's career—connecting daily spending decisions to a deeper purpose makes short-term sacrifice feel meaningful.

Celebrate Small Wins

Reached your starter emergency fund goal? Celebrate with a modest, budgeted treat. Paid off your credit card? Acknowledge the achievement. These celebrations reinforce positive behaviour and make the journey sustainable.

Automate Savings and Minimum Payments

Automate everything possible: retirement contributions, emergency fund deposits, and minimum debt payments. Automation removes decision fatigue and ensures your financial priorities are funded before you have the chance to spend money elsewhere.

Build Rewards into the Budget

Dedicating 15–20% of your income to wants means you never have to feel guilty about a coffee out or a movie night. The budget is designed to include enjoyment—define what enjoyment looks like for your family and allocate to it without apology.

Revisit and Adjust Quarterly

Life changes. A budget that worked two years ago may not fit your current reality. Revisit your budget quarterly and adjust categories, targets, and priorities as needed. Flexibility is what keeps budgets working rather than breaking.

Connect with Others in the Same Situation

Join online communities, local meetups, or social media groups for single-income families. Sharing challenges, tips, and encouragement with others on the same path reduces isolation and provides practical ideas you may not have discovered alone.

Frequently Asked Questions

Is it realistic to live on one income in 2026?

Yes, millions of families thrive on a single income by using zero-based budgeting, the 50/30/20 rule adapted for one earner, and intentional spending strategies. The key is living below your means and prioritizing needs over wants. Families who budget intentionally typically report less financial stress than dual-income households that live paycheck to paycheck.

What percentage of income should go to housing on one salary?

Financial experts recommend keeping housing costs to 25–30% of your gross income. For a single-income household, this ensures enough is left for savings, utilities, maintenance, insurance, and other essential expenses without stretching the budget too thin.

How do single-income couples handle unexpected expenses?

A fully funded emergency fund covering 3–6 months of expenses is the foundation. Building this fund takes time, so in the interim, maintaining a dedicated backup fund and having access to a low-interest credit line for genuine emergencies is practical. Never rely on credit cards as your primary emergency response.

Should both partners contribute to household finances if one earns?

Absolutely. The earning spouse brings home the paycheck, but both partners should participate in budgeting decisions, tracking spending, and financial planning. Many couples find that a written partnership agreement clarifies expectations and reduces tension around money management.

What is the best budgeting method for one-income households?

Zero-based budgeting where every dollar has a job before the month begins is widely regarded as the most effective for single-income families. Envelope budgeting for discretionary categories and the 50/30/20 rule adapted for one earner are also excellent options. Choose the method you will actually use consistently.

Can a one-income family afford to save for retirement?

Yes, and it is critical. Single-income families should aim to save 15–20% of the primary earner's gross income in tax-advantaged retirement accounts like a 401(k) and Roth IRA. Compound growth over decades dramatically increases long-term wealth, and starting early—even with modest amounts—makes an enormous difference over a 30–40 year career.

How do I cut costs without feeling deprived on a single income?

Focus on high-impact reductions: dining out less, cancelling unused subscriptions, negotiating bills, switching to generic brands, and cooking more meals at home. These sacrifices often save thousands per year with minimal impact on quality of life. The goal is not deprivation—it is intentionality.

Life insurance for single-income families: how much is enough?

A general rule is 10–12 times the primary earner's annual income, plus coverage for any outstanding debts, mortgage, and children's education costs. Term life insurance provides the most protection at an affordable cost for most families. Review coverage every 3–5 years as income, assets, and family circumstances change.

Sources & Methodology

-

U.S. Census Bureau — Historical Income Statistics — Used to establish the prevalence of single-income households in the United States.

-

Australian Bureau of Statistics — Household Income and Wealth — Data on Australian household income distribution and single-income family statistics.

-

Financial Resilience Institute — Financial Resilience Survey 2025 — Research findings on budget adoption and financial security outcomes for single-income families.

-

Consumer Financial Protection Bureau — Managing a Household Budget — Federal guidance on budgeting methodology and zero-based budgeting principles.

-

Moneysmart.gov.au — Superannuation and Retirement Planning — Australian government financial guidance for retirement savings and superannuation optimisation.

-

National Association of Personal Financial Advisors (NAPFA) — Professional standards for fee-only financial advisors providing guidance on insurance and retirement planning.

-

Australian Securities and Investments Commission (ASIC) — MoneySmart — Information on savings strategies, emergency fund building, and debt management for Australian households.

This article was written by Sarah Mitchell, a Certified Financial Planner with over 12 years of experience advising couples and families on budgeting, debt management, and long-term financial planning. Sarah holds a Graduate Diploma in Financial Planning from the University of Melbourne and is a member of the Financial Planning Association of Australia.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a licensed financial planner or advisor before making significant financial decisions.