Couples Budgeting

How to Build an Emergency Fund as a Couple (2026)

Learn how to build an emergency fund as a couple in 2026. Step-by-step guide covering savings targets, contribution splits, and where to keep your joint fund.

Building an emergency fund as a couple means agreeing on a shared savings target, deciding how to split contributions fairly, and keeping the money somewhere it earns interest but stays accessible. Most couples need 3–6 months of household expenses — and a clear written definition of what "emergency" actually means before they need it.

By Rachel Torres, Certified Financial Education Instructor (CFEI) | Last updated: April 2026

Table of Contents

- Why Couples Need a Dedicated Emergency Fund

- How Much Should a Couple Save? Setting Your Target

- Step-by-Step: Building Your Emergency Fund Together

- Where to Keep Your Joint Emergency Fund

- How to Split Contributions When Incomes Are Unequal

- What Counts as a Real Emergency?

- Rebuilding After You Tap the Fund

- FAQ: Emergency Funds for Couples

- Sources and Methodology

Why Couples Need a Dedicated Emergency Fund

Most conversations about emergency funds are written for individuals. But building a financial safety net as a couple is fundamentally different — and more complicated — than saving solo.

When you share a household, you share financial risk. One partner losing their job doesn't just affect their personal finances; it destabilises the entire household's ability to cover rent, utilities, groceries, and debt payments. A single medical emergency can threaten a shared mortgage. A broken-down car that one partner uses to get to work is both partners' problem.

According to the Federal Reserve's 2023 Survey of Household Economics and Decisionmaking (SHED), approximately 37% of U.S. adults would not be able to cover an unexpected $400 expense using cash or its equivalent without borrowing or selling something. For couples, that number is lower — but the size of potential emergencies is significantly larger when you factor in combined household expenses.

The Risks of Relying on Only One Partner's Savings

A common mistake couples make is assuming one partner's existing emergency fund will cover both of them. It usually won't. Individual emergency funds are sized for individual expenses — a single person's rent, a single person's food costs, a single person's insurance premiums. Once you combine households, your shared monthly expenses often double, while one person's savings buffer stays the same.

The other trap is the informal approach: "we'll figure it out together." This works until it doesn't. When a true emergency hits, financial stress is one of the fastest ways to damage a relationship. The American Psychological Association's Stress in America surveys consistently identify money as a top source of relationship conflict. Having a funded emergency account removes that pressure point before it becomes a crisis.

Why Couples Are Actually Better Positioned to Build One

Here's the good news: couples have a structural advantage over individuals. Two incomes mean two streams of cash flowing toward a shared savings goal. If one partner loses their job, the other's income provides a bridge. If both contribute consistently, the fund builds faster than either could achieve alone.

The goal is to harness that advantage intentionally — not leave it to chance.

How Much Should a Couple Save? Setting Your Target

The standard rule is 3–6 months of living expenses. For couples, the right number depends on your specific situation. Here's how to think about it:

Monthly expenses to include in your calculation:

- Rent or mortgage payment

- Utilities (electricity, gas, water, internet, phone)

- Groceries and household supplies

- Insurance premiums (health, car, renters/homeowners)

- Minimum debt payments (credit cards, student loans, car loans)

- Transportation costs (gas, public transit, car maintenance)

- Childcare or pet care costs

- Any subscription services you'd keep during a crisis

Do not include discretionary spending like dining out, entertainment, or clothing. Your emergency fund covers survival-level expenses, not lifestyle maintenance.

Couple Emergency Fund Size Comparison by Situation

| Couple Type | Recommended Target | Reasoning |

|---|---|---|

| Dual income, both salaried, no dependants | 3 months expenses | Lower risk — two stable incomes provide natural backup |

| Dual income, one or both with variable pay | 4–6 months expenses | Commission or freelance income can drop suddenly |

| Single income household | 6–9 months expenses | Entire household depends on one earner; buffer must be larger |

| Self-employed (one or both partners) | 6–12 months expenses | Business downturns affect personal finances directly |

| Dual income with children or dependants | 5–6 months expenses | More financial obligations; less flexibility to cut spending fast |

| Recent major purchase (home, car) | 4–6 months expenses | New large assets bring new repair/maintenance risk |

| Approaching retirement | 6 months + expenses | Sequence-of-returns risk; want to avoid selling investments |

A Simple Formula

- Add up your total monthly household expenses (the list above)

- Multiply by your target number of months (from the table above)

- That's your emergency fund goal

Example: A couple with $5,800/month in combined household expenses, both salaried employees with no children, needs between $17,400 (3 months) and $34,800 (6 months). A reasonable starting milestone is $17,400, with a stretch goal of $26,100 (4.5 months).

Don't let the final number paralyse you. You don't need to hit it overnight. The goal is to have a target and make measurable progress toward it.

Step-by-Step: Building Your Emergency Fund Together

Building an emergency fund is straightforward in theory. The challenge for couples is doing it together — aligning on the goal, agreeing on how to get there, and maintaining the discipline over months or years. Here is a practical six-step process.

Step 1: Have the Money Conversation First

Before you open any account or set up any transfer, sit down together and get aligned. This conversation needs to cover:

- Why this matters to both of you. What's the fear or event that makes an emergency fund feel urgent? Voicing this makes the goal feel real and shared.

- What dollar amount you're targeting. Use the formula above to calculate your number together.

- What timeline you're working with. Be realistic — if you're starting from zero and your target is $20,000, that's 18–24 months at most realistic savings rates.

If money conversations tend to turn tense in your relationship, the article on how to have a money talk without fighting walks through a framework for keeping these discussions productive rather than combative.

Step 2: Do a Spending Audit to Find Your Monthly Savings Capacity

You can't save what you haven't found. Before deciding on a monthly contribution amount, both partners need visibility into current cash flow.

Pull three months of bank and credit card statements. Categorise every expense into:

- Fixed essential (rent, insurance, loan minimums)

- Variable essential (groceries, gas, utilities)

- Discretionary (dining, entertainment, subscriptions, shopping)

The gap between your combined take-home pay and your fixed + variable essential spending is your theoretical savings capacity. Your target emergency fund contribution should come out of that gap — before discretionary spending is allocated.

Using a budgeting app makes this audit much faster. The best budgeting apps for couples reviewed on this site include tools that automatically categorise transactions and show both partners' spending in one dashboard.

Step 3: Open a Dedicated Joint High-Yield Savings Account

Your emergency fund needs a home that is:

- Separate from your everyday checking account — out of sight, out of temptation

- Earning meaningful interest — a standard savings account at a big bank typically pays 0.01%–0.10% APY; an online high-yield savings account can pay 4.00%–5.00% APY

- Accessible within 1–2 business days — not locked in a CD or investment account

- FDIC insured — protecting up to $250,000 per depositor per institution

Popular joint high-yield savings account options as of 2026 include Ally Bank, Marcus by Goldman Sachs, and SoFi. All three offer competitive APYs, no minimum balance requirements, and joint account capability.

For books that go deeper on structuring your joint finances, I Will Teach You to Be Rich by Ramit Sethi is an excellent practical guide available on Amazon — it covers the exact account setup system for couples in detail.

Step 4: Set a Monthly Contribution and Automate It

Decide on a specific dollar amount to transfer to the emergency fund each month. Automation is non-negotiable: manual transfers get skipped when life gets busy, and willpower is an unreliable budgeting strategy.

Set up an automatic transfer from your joint checking account to your emergency fund savings account to execute on the same day each month — ideally the day after your combined paydays hit.

A realistic contribution target:

- Starter rate (tight budget): $200–$400/month

- Moderate rate (comfortable budget): $500–$800/month

- Aggressive rate (high priority): $1,000–$1,500+/month

Even $300/month builds a $3,600 buffer in 12 months — enough to cover most individual-level emergencies and meaningful protection against unexpected expenses.

The 50/30/20 budget rule for couples allocates 20% of after-tax income to savings and debt. If you apply that framework, your emergency fund contributions come out of this 20% bucket until the fund is fully funded — then that allocation shifts to other financial goals like investing or saving for a house.

Step 5: Accelerate With Windfalls

Regular contributions build the fund steadily. Windfalls build it fast. Agree in advance on what percentage of unexpected money goes directly to the emergency fund:

- Tax refunds

- Work bonuses

- Inheritance or gifts

- Money from selling unwanted items

- Freelance or side income

A common couple's rule: 50% of any windfall goes to the emergency fund until fully funded. The other 50% goes wherever feels right — a trip, a dinner out, a shared fun purchase. This keeps the rule sustainable without making it feel punishing.

Step 6: Define "Emergency" Together — In Writing

This step is overlooked by nearly every couple and is the source of the most emergency fund conflict. If you don't have a shared definition of what qualifies as an emergency, one partner will raid the fund for something the other considers unnecessary.

Write it down together. Keep it somewhere both partners can reference it — a shared note, your budgeting app, a sticky note on the fridge.

Where to Keep Your Joint Emergency Fund

The best account for a couples' emergency fund is a joint high-yield savings account (HYSA) at an FDIC-insured institution. Here's why each attribute matters:

Joint vs Individual Accounts

A joint account gives both partners equal access and visibility. This matters for emergencies — you don't want one partner unable to access funds in a crisis because the account is in the other person's name only.

For more context on how joint accounts fit into a couple's broader financial structure, the comparison on joint bank account vs separate accounts covers the tradeoffs in detail.

High-Yield vs Regular Savings

The interest rate difference between a traditional bank savings account and an online HYSA is not trivial. On a $20,000 balance:

- Traditional savings at 0.05% APY: ~$10/year interest

- Online HYSA at 4.50% APY: ~$900/year interest

That $890 annual difference is money working for you while it sits waiting. Over the 2–3 years most couples take to fully fund their emergency account, the compound effect is meaningful.

Keeping It Separate From Day-to-Day Accounts

The behavioural benefit of a separate account is underrated. When your emergency fund lives in the same account you pay bills from, it becomes mentally part of your "available balance" — and it gets spent. A separate account, especially one that requires a 1–2 day transfer window to access, creates just enough friction to prevent impulsive withdrawals.

Building good financial habits together takes consistency. Tracking your daily savings habits with a tool like HabitTrackerSpot can help both partners stay accountable to their contribution goals between monthly budget reviews.

What to Avoid

- Money market funds: Not FDIC insured; fine for investing, wrong tool for emergency savings

- CDs (certificates of deposit): Locks your money for a fixed term; emergency access means paying early withdrawal penalties

- Investment accounts: Subject to market volatility; a $20,000 fund can become $14,000 in a downturn right when you need it most

- Cash at home: No interest, no FDIC protection, and not practical above a few hundred dollars

How to Split Contributions When Incomes Are Unequal

Income inequality is the most common source of tension in couples' budgeting. When one partner earns significantly more than the other, deciding how to split emergency fund contributions requires a clear framework.

The Two Main Models

Equal dollar contributions: Both partners contribute the same amount each month — say, $400 each, regardless of income.

Advantage: Simple and easy to track. Disadvantage: Creates financial stress for the lower earner. Paying $400/month when you earn $3,000 is a 13% income share; paying $400/month when you earn $6,000 is only 6.7%. The sacrifice is unequal even though the dollar amounts are identical.

Proportional contributions (recommended): Each partner contributes a percentage of their income equal to the household savings rate.

Example: The household target is to save $1,000/month toward the emergency fund. Partner A earns 65% of combined household income; Partner B earns 35%. Partner A contributes $650/month; Partner B contributes $350/month.

Advantage: Both partners sacrifice the same proportion of their income. This feels fair and sustainable.

When One Partner Is Not Currently Earning

One partner may be taking parental leave, studying, or between jobs. In this case, the earning partner covers 100% of contributions temporarily, with a clear expectation that contributions will rebalance when the non-earning partner returns to income.

Making this explicit — rather than leaving it as an unspoken assumption — prevents resentment from building on both sides.

Protecting Individual Financial Agency

Even in a fully merged financial model, consider allowing each partner a small personal emergency buffer — $500 to $1,000 in their own individual account — for genuinely personal unexpected expenses (a personal medical cost, a family situation the other partner doesn't need to be part of). This isn't secrecy; it's reasonable individual autonomy within a joint financial framework.

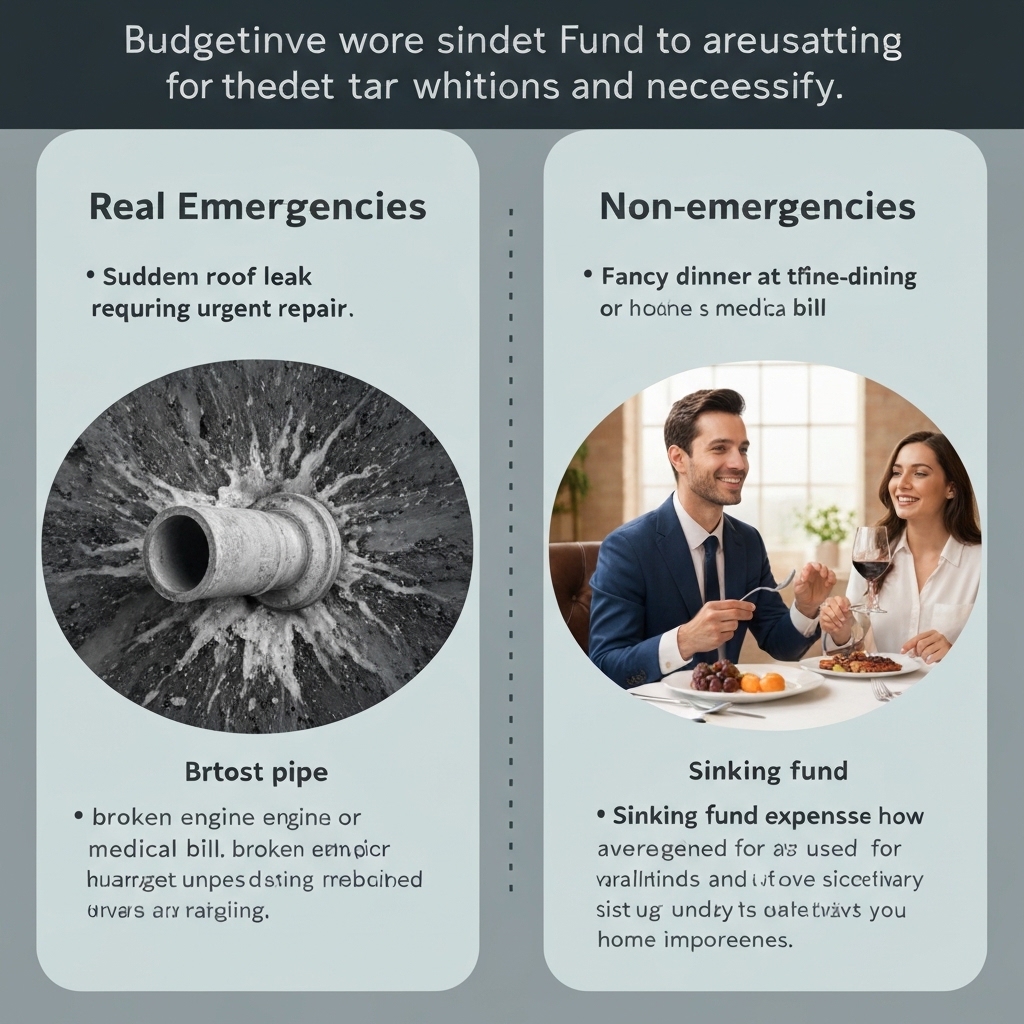

What Counts as a Real Emergency?

The emergency fund conversation that never happens is the one about what the fund is actually for. Without a shared definition, one partner will eventually withdraw funds for something the other considers non-essential — and trust in the system breaks down.

True Emergencies: The Fund Is for These

- Job loss: Either partner loses income unexpectedly. The fund covers household expenses while the search for new work happens.

- Medical or dental emergencies: Unexpected illness, injury, or urgent dental work not covered by insurance.

- Critical car repairs: The car stops working and is needed to get to work. Not a worn tyre or scheduled service — a transmission failure, engine problem, or accident repair.

- Urgent home repairs: A burst pipe, failed heating in winter, or structural damage that cannot be safely deferred.

- Family crisis: A death or illness in the family requiring emergency travel or temporary financial support.

What Is NOT an Emergency

- A flight sale you don't want to miss

- Holiday gifts or birthday presents

- Car registration, annual insurance premiums, or tax bills (these are predictable — they belong in a sinking fund)

- A sale on furniture or electronics you've been wanting

- A planned home renovation

- An upgrade to your phone or laptop

Predictable annual expenses are not emergencies — they're just infrequent costs. If you find yourself using the emergency fund for these, the real problem is that you haven't built sinking funds for planned irregular expenses. This is a budgeting structure issue, not an emergency issue.

Write your definition together. A sample joint definition:

"Our emergency fund is for unplanned expenses that are urgent, necessary for maintaining our housing/employment/health, and cannot reasonably be deferred. Both partners must agree before any withdrawal above $200."

The two-partner agreement rule for larger withdrawals is particularly important — it prevents unilateral decisions and ensures the fund is protected even under pressure.

If you're saving for a large planned goal alongside your emergency fund, the article on saving for a house as a couple explains how to structure both goals simultaneously without underfunding either.

Rebuilding After You Tap the Fund

Using your emergency fund is not a failure — it's exactly what it's there for. The risk is failing to replenish it promptly. A depleted fund leaves you exposed if another emergency hits before you've rebuilt.

The Rebuilding Plan: Three Steps

Step 1: Acknowledge and assess. As soon as the immediate crisis is resolved, sit down together and assess the damage. How much was withdrawn? What's the current balance? How far from your target are you?

Step 2: Set a rebuild timeline. Treat the rebuild exactly like the original build: set a monthly contribution amount and automate it. Consider temporarily increasing contributions during the rebuild phase — for example, if your regular contribution was $500/month, push it to $800/month until the fund is restored.

Step 3: Don't redirect savings until the fund is fully restored. It's tempting, once the emergency has passed, to return to other financial priorities — investing, saving for a holiday, paying down debt faster. Resist this. The emergency fund restores first. Everything else waits.

The Psychological Side

There's often guilt or anxiety after depleting an emergency fund, especially if one partner feels the other "caused" the emergency. Be deliberate about reframing this: the fund existed precisely to be used. The fact that you had it meant the emergency didn't become a debt spiral or a relationship crisis. That's a financial win, not a failure.

Set a rebuild milestone — a balance you're both working toward — and celebrate when you hit it. A fully replenished emergency fund is one of the most concrete financial achievements a couple can reach together.

FAQ: Emergency Funds for Couples

How much should a couple have in an emergency fund?

Most financial planners recommend 3–6 months of combined household expenses. A couple spending $5,000 per month should aim for $15,000–$30,000. Couples with variable income, self-employment, or a single-income household should target the higher end: 6–9 months of expenses. Start with a $1,000 starter fund as your first milestone, then build from there.

Should couples have a joint or separate emergency fund?

A single joint emergency fund is the most practical approach for most couples. It pools resources for a faster build, and a shared fund covers shared expenses — rent, utilities, food — more efficiently than two separate smaller funds. That said, each partner keeping a small personal buffer of $500–$1,000 for individual unexpected costs is reasonable and doesn't undermine the shared goal.

How do couples split emergency fund contributions fairly?

Proportional contribution based on income is the fairest approach. If Partner A earns 60% of household income, they contribute 60% of the monthly savings target. This ensures both partners sacrifice the same percentage of their income rather than the same dollar amount — which matters significantly when incomes are unequal.

Where should couples keep their emergency fund?

A high-yield savings account (HYSA) at an FDIC-insured online bank is the best home for a couples' emergency fund. Look for APY rates above 4%, no monthly fees, and easy online access for both account holders. Keep it at a different bank than your everyday checking to reduce the temptation to dip into it for non-emergencies.

What qualifies as an emergency fund emergency?

True emergencies are unexpected, necessary, and urgent: job loss, medical bills, critical car or home repairs, or a family crisis requiring emergency travel. Planned expenses like holidays, annual car registration, or known subscription renewals are not emergencies — those belong in dedicated sinking funds. Create a written definition together before you need it.

How long does it take a couple to build a full emergency fund?

At a combined $1,000/month savings rate, a $20,000 emergency fund target takes 20 months. Directing windfalls like tax refunds toward the fund, and temporarily increasing contributions after a pay rise, can cut this to 12–15 months for many couples. The most important factor is consistency: automated monthly contributions outperform larger irregular deposits over the long term.

Sources and Methodology

This article draws on data and guidance from the following sources:

-

Board of Governors of the Federal Reserve System. "Report on the Economic Well-Being of U.S. Households in 2022" (SHED). Published May 2023. Available at: federalreserve.gov/consumerscommunities/shed.htm

-

Consumer Financial Protection Bureau (CFPB). "Financial Well-Being in America." Published 2017, supplemental data updated 2023. Available at: consumerfinance.gov/data-research/financial-well-being-survey-data

-

Bankrate. "Annual Emergency Savings Report 2025." Data covers savings habits, emergency fund adequacy, and financial resilience across U.S. households. Available at: bankrate.com

-

Bureau of Labor Statistics, U.S. Department of Labor. "Consumer Expenditure Survey (CE), 2022–2023." Provides household spending benchmark data used to estimate emergency fund targets. Available at: bls.gov/cex

-

American Psychological Association. "Stress in America 2023: A Nation Recovering from Collective Trauma." Includes data on financial stress as a driver of relationship conflict. Available at: apa.org/news/press/releases/stress

-

FDIC (Federal Deposit Insurance Corporation). "2023 FDIC National Survey of Unbanked and Underbanked Households." Data on account access and savings vehicle usage. Available at: fdic.gov/householdsurvey

Methodology note: Emergency fund recommendations in this article are based on standard financial planning guidance from CFPB, the National Endowment for Financial Education (NEFE), and fee-only certified financial planners. All income and expense examples are illustrative and do not represent specific individuals.

About the author: Rachel Torres is a Certified Financial Education Instructor (CFEI) with over eight years of experience writing about personal finance, couples budgeting, and household financial planning. She specialises in making financial concepts accessible to couples navigating shared money decisions for the first time.